Advertisement

The CEO of Nameson Holdings Limited (HKG:1982) is Ting Chung Wong, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

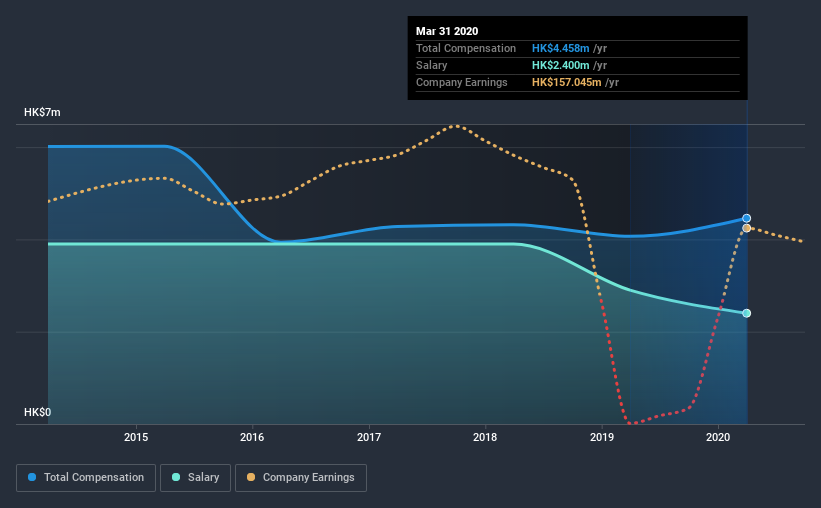

See our latest analysis for Nameson Holdings

How Does Total Compensation For Ting Chung Wong Compare With Other Companies In The Industry?

Our data indicates that Nameson Holdings Limited has a market capitalization of HK$1.0b, and total annual CEO compensation was reported as HK$4.5m for the year to March 2020. That's a notable increase of 9.6% on last year. In particular, the salary of HK$2.40m, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$2.4m. Accordingly, our analysis reveals that Nameson Holdings Limited pays Ting Chung Wong north of the industry median. Furthermore, Ting Chung Wong directly owns HK$757m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | HK$2.4m | HK$2.9m | 54% |

| Other | HK$2.1m | HK$1.2m | 46% |

| Total Compensation | HK$4.5m | HK$4.1m | 100% |

Talking in terms of the industry, salary represented approximately 93% of total compensation out of all the companies we analyzed, while other remuneration made up 7.3% of the pie. It's interesting to note that Nameson Holdings allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Nameson Holdings Limited's Growth

Over the last three years, Nameson Holdings Limited has shrunk its earnings per share by 34% per year. Its revenue is down 17% over the previous year.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Nameson Holdings Limited Been A Good Investment?

Given the total shareholder loss of 83% over three years, many shareholders in Nameson Holdings Limited are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we noted earlier, Nameson Holdings pays its CEO higher than the norm for similar-sized companies belonging to the same industry. Disappointingly, share price gains over the last three years have failed to materialize. Arguably worse, we've been waiting for positive EPS growth for the last three years. Considering such poor performance, we think shareholders might be concerned if the CEO's compensation were to grow.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 3 warning signs for Nameson Holdings that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Nameson Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nameson Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1982

Nameson Holdings

Manufactures and sells knitwear products in Japan, North America, Europe, Mainland China, Southeast Asia, and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative