Increases to CEO Compensation Might Be Put On Hold For Now at Justin Allen Holdings Limited (HKG:1425)

Key Insights

- Justin Allen Holdings to hold its Annual General Meeting on 20th of June

- Salary of HK$1.32m is part of CEO Edmond Tam's total remuneration

- The overall pay is 52% above the industry average

- Justin Allen Holdings' total shareholder return over the past three years was 64% while its EPS grew by 2.5% over the past three years

Under the guidance of CEO Edmond Tam, Justin Allen Holdings Limited (HKG:1425) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 20th of June. However, some shareholders will still be cautious of paying the CEO excessively.

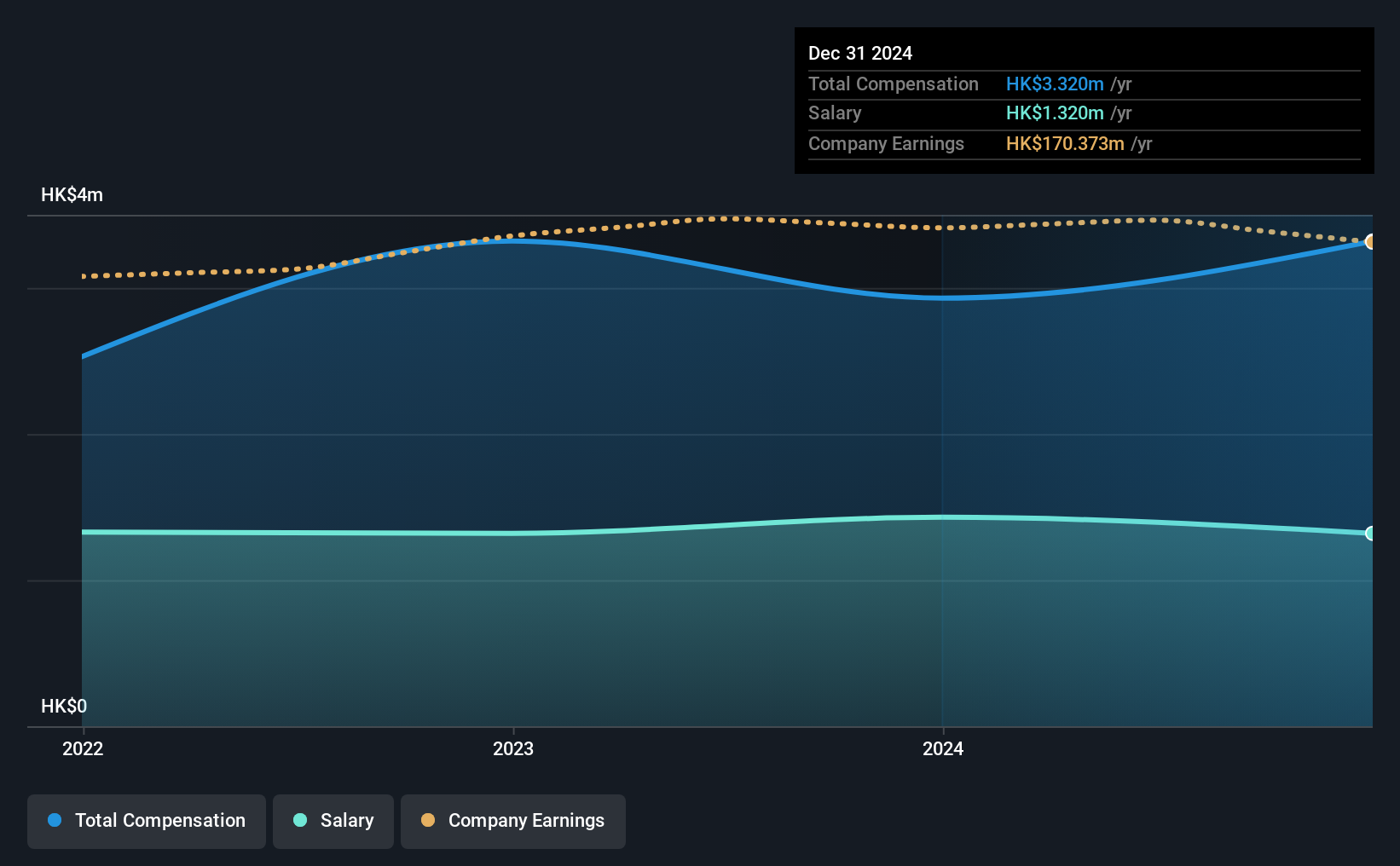

Check out our latest analysis for Justin Allen Holdings

How Does Total Compensation For Edmond Tam Compare With Other Companies In The Industry?

At the time of writing, our data shows that Justin Allen Holdings Limited has a market capitalization of HK$913m, and reported total annual CEO compensation of HK$3.3m for the year to December 2024. That's a notable increase of 13% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at HK$1.3m.

On comparing similar-sized companies in the Hong Kong Luxury industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was HK$2.2m. Accordingly, our analysis reveals that Justin Allen Holdings Limited pays Edmond Tam north of the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$1.3m | HK$1.4m | 40% |

| Other | HK$2.0m | HK$1.5m | 60% |

| Total Compensation | HK$3.3m | HK$2.9m | 100% |

Speaking on an industry level, nearly 89% of total compensation represents salary, while the remainder of 11% is other remuneration. Justin Allen Holdings pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Justin Allen Holdings Limited's Growth Numbers

Over the past three years, Justin Allen Holdings Limited has seen its earnings per share (EPS) grow by 2.5% per year. It saw its revenue drop 4.2% over the last year.

We would prefer it if there was revenue growth, but the modest improvement in EPS is good. It's hard to reach a conclusion about business performance right now. This may be one to watch. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Justin Allen Holdings Limited Been A Good Investment?

We think that the total shareholder return of 64%, over three years, would leave most Justin Allen Holdings Limited shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for Justin Allen Holdings that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1425

Justin Allen Holdings

An investment holding company, manufactures and sells sleepwear and loungewear products in the People’s Republic of China, the United States of America, the United Kingdom, Ireland, Canada, and Spain.

Flawless balance sheet and good value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion