How Much Is Guangdong Tannery's (HKG:1058) CEO Getting Paid?

Jun Sun has been the CEO of Guangdong Tannery Limited (HKG:1058) since 2010, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for Guangdong Tannery

Comparing Guangdong Tannery Limited's CEO Compensation With the industry

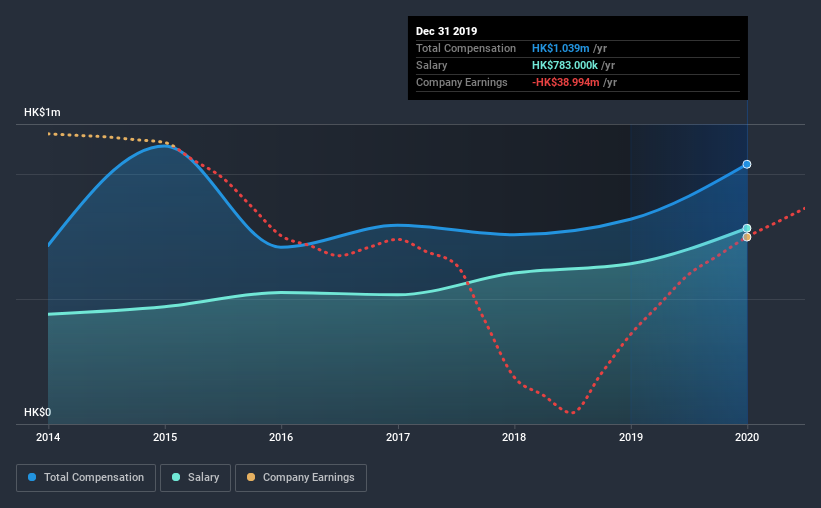

According to our data, Guangdong Tannery Limited has a market capitalization of HK$175m, and paid its CEO total annual compensation worth HK$1.0m over the year to December 2019. Notably, that's an increase of 27% over the year before. We note that the salary portion, which stands at HK$783.0k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$2.4m. That is to say, Jun Sun is paid under the industry median.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | HK$783k | HK$641k | 75% |

| Other | HK$256k | HK$178k | 25% |

| Total Compensation | HK$1.0m | HK$819k | 100% |

Talking in terms of the industry, salary represented approximately 93% of total compensation out of all the companies we analyzed, while other remuneration made up 7.4% of the pie. It's interesting to note that Guangdong Tannery allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Guangdong Tannery Limited's Growth Numbers

Over the past three years, Guangdong Tannery Limited has seen its earnings per share (EPS) grow by 30% per year. In the last year, its revenue is down 40%.

Shareholders would be glad to know that the company has improved itself over the last few years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Guangdong Tannery Limited Been A Good Investment?

Since shareholders would have lost about 59% over three years, some Guangdong Tannery Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be lessto generous with CEO compensation.

In Summary...

As previously discussed, Jun is compensated less than what is normal for CEOs of companies of similar size, and which belong to the same industry. However, the EPS growth over three years is certainly impressive. Considering EPS are on the up, we would say Jun is compensated fairly. Shareholders, though, would ideally like to see shareholder returns head north before they agree to any raise.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 2 warning signs (and 1 which doesn't sit too well with us) in Guangdong Tannery we think you should know about.

Switching gears from Guangdong Tannery, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Guangdong Tannery, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Namyue Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1058

Namyue Holdings

An investment holding company, engages in the processing and sale of semi-finished and finished leather in Mainland China.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives