Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:8416

Here's Why Shareholders Will Not Be Complaining About HM International Holdings Limited's (HKG:8416) CEO Pay Packet

Key Insights

- HM International Holdings' Annual General Meeting to take place on 9th of May

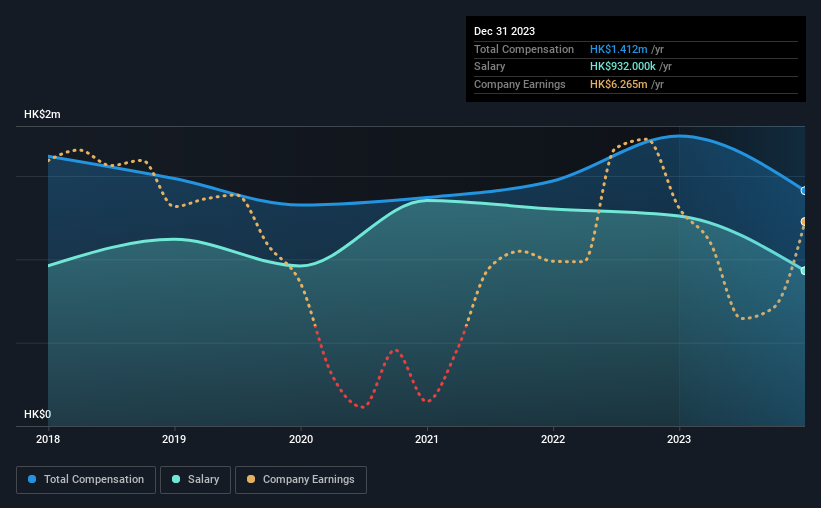

- CEO Wai Lin Chan's total compensation includes salary of HK$932.0k

- The total compensation is similar to the average for the industry

- HM International Holdings' EPS grew by 36% over the past three years while total shareholder return over the past three years was 34%

We have been pretty impressed with the performance at HM International Holdings Limited (HKG:8416) recently and CEO Wai Lin Chan deserves a mention for their role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 9th of May. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. Here is our take on why we think CEO compensation is not extravagant.

View our latest analysis for HM International Holdings

How Does Total Compensation For Wai Lin Chan Compare With Other Companies In The Industry?

At the time of writing, our data shows that HM International Holdings Limited has a market capitalization of HK$43m, and reported total annual CEO compensation of HK$1.4m for the year to December 2023. Notably, that's a decrease of 19% over the year before. Notably, the salary which is HK$932.0k, represents most of the total compensation being paid.

For comparison, other companies in the Hong Kong Commercial Services industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$1.9m. From this we gather that Wai Lin Chan is paid around the median for CEOs in the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$932k | HK$1.3m | 66% |

| Other | HK$480k | HK$480k | 34% |

| Total Compensation | HK$1.4m | HK$1.7m | 100% |

Speaking on an industry level, nearly 80% of total compensation represents salary, while the remainder of 20% is other remuneration. HM International Holdings sets aside a smaller share of compensation for salary, in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

HM International Holdings Limited's Growth

HM International Holdings Limited's earnings per share (EPS) grew 36% per year over the last three years. Its revenue is down 6.1% over the previous year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. While it would be good to see revenue growth, profits matter more in the end. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has HM International Holdings Limited Been A Good Investment?

Boasting a total shareholder return of 34% over three years, HM International Holdings Limited has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 4 warning signs for HM International Holdings you should be aware of, and 1 of them shouldn't be ignored.

Important note: HM International Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if HM International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8416

HM International Holdings

An investment holding company, provides integrated printing services in Hong Kong.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor