Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:8128

China Geothermal Industry Development Group (HKG:8128) Has Debt But No Earnings; Should You Worry?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that China Geothermal Industry Development Group Limited (HKG:8128) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China Geothermal Industry Development Group

How Much Debt Does China Geothermal Industry Development Group Carry?

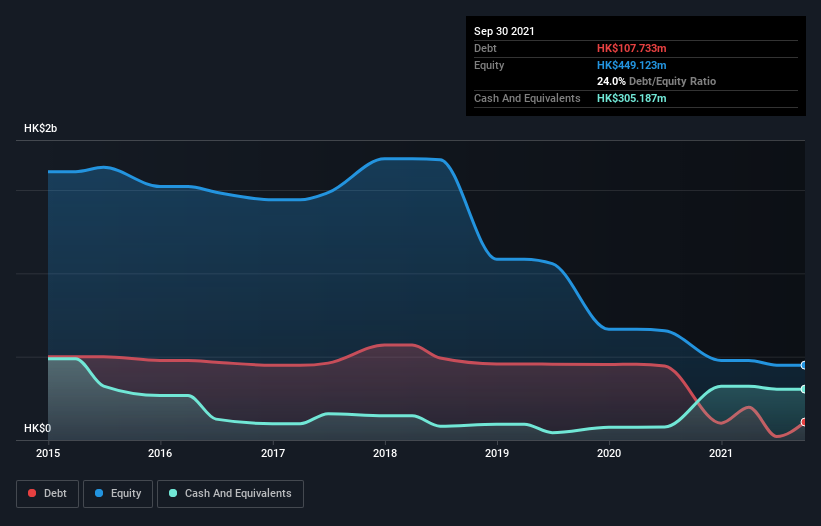

You can click the graphic below for the historical numbers, but it shows that China Geothermal Industry Development Group had HK$107.7m of debt in June 2021, down from HK$443.9m, one year before. However, it does have HK$305.2m in cash offsetting this, leading to net cash of HK$197.5m.

How Strong Is China Geothermal Industry Development Group's Balance Sheet?

We can see from the most recent balance sheet that China Geothermal Industry Development Group had liabilities of HK$1.06b falling due within a year, and liabilities of HK$129.4m due beyond that. Offsetting these obligations, it had cash of HK$305.2m as well as receivables valued at HK$186.9m due within 12 months. So its liabilities total HK$697.0m more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the HK$398.4m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, China Geothermal Industry Development Group would likely require a major re-capitalisation if it had to pay its creditors today. Given that China Geothermal Industry Development Group has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. The balance sheet is clearly the area to focus on when you are analysing debt. But it is China Geothermal Industry Development Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year China Geothermal Industry Development Group had a loss before interest and tax, and actually shrunk its revenue by 45%, to HK$171m. To be frank that doesn't bode well.

So How Risky Is China Geothermal Industry Development Group?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year China Geothermal Industry Development Group had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of HK$73m and booked a HK$271m accounting loss. But at least it has HK$197.5m on the balance sheet to spend on growth, near-term. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for China Geothermal Industry Development Group (1 shouldn't be ignored!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8128

CHYY Development Group

An investment holding company, engages in the research, development, and promotion of geothermal energy as alternative energy for building’s heating applications in the People's Republic of China.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor