- Hong Kong

- /

- Commercial Services

- /

- SEHK:1975

Sun Hing Printing Holdings's (HKG:1975) Earnings Are Growing But Is There More To The Story?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. Today we'll focus on whether this year's statutory profits are a good guide to understanding Sun Hing Printing Holdings (HKG:1975).

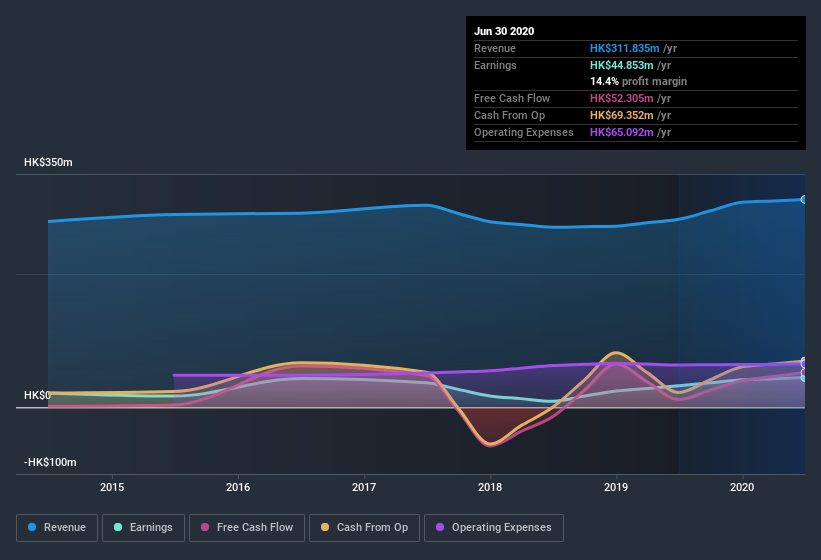

While Sun Hing Printing Holdings was able to generate revenue of HK$311.8m in the last twelve months, we think its profit result of HK$44.9m was more important. In the chart below, you can see that its profit and revenue have both grown over the last three years.

View our latest analysis for Sun Hing Printing Holdings

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Sun Hing Printing Holdings' statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Sun Hing Printing Holdings.

How Do Unusual Items Influence Profit?

Importantly, our data indicates that Sun Hing Printing Holdings' profit was reduced by HK$9.0m, due to unusual items, over the last year. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And that's hardly a surprise given these line items are considered unusual. If Sun Hing Printing Holdings doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Sun Hing Printing Holdings' Profit Performance

Because unusual items detracted from Sun Hing Printing Holdings' earnings over the last year, you could argue that we can expect an improved result in the current quarter. Because of this, we think Sun Hing Printing Holdings' earnings potential is at least as good as it seems, and maybe even better! And the EPS is up 39% over the last twelve months. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Sun Hing Printing Holdings, you'd also look into what risks it is currently facing. You'd be interested to know, that we found 2 warning signs for Sun Hing Printing Holdings and you'll want to know about these.

Today we've zoomed in on a single data point to better understand the nature of Sun Hing Printing Holdings' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you’re looking to trade Sun Hing Printing Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Sun Hing Printing Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1975

Sun Hing Printing Holdings

An investment holding company, manufactures and sells printing products in Hong Kong, Mainland China, Rest of Asia, Europe, the United States, Oceania, and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Community Narratives