Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:1650

Hygieia Group's (HKG:1650) Soft Earnings Are Actually Better Than They Appear

The market for Hygieia Group Limited's (HKG:1650) shares didn't move much after it posted weak earnings recently. We think that the softer headline numbers might be getting counterbalanced by some positive underlying factors.

See our latest analysis for Hygieia Group

A Closer Look At Hygieia Group's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

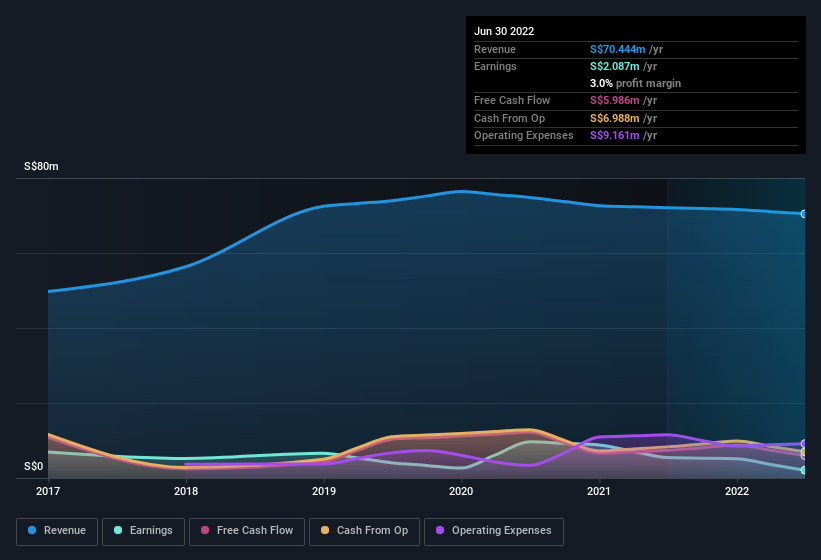

Hygieia Group has an accrual ratio of -0.29 for the year to June 2022. Therefore, its statutory earnings were very significantly less than its free cashflow. In fact, it had free cash flow of S$6.0m in the last year, which was a lot more than its statutory profit of S$2.09m. Hygieia Group's free cash flow actually declined over the last year, which is disappointing, like non-biodegradable balloons. However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Hygieia Group.

How Do Unusual Items Influence Profit?

While the accrual ratio might bode well, we also note that Hygieia Group's profit was boosted by unusual items worth S$875k in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. We can see that Hygieia Group's positive unusual items were quite significant relative to its profit in the year to June 2022. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Hygieia Group's Profit Performance

Hygieia Group's profits got a boost from unusual items, which indicates they might not be sustained and yet its accrual ratio still indicated solid cash conversion, which is promising. Based on these factors, it's hard to tell if Hygieia Group's profits are a reasonable reflection of its underlying profitability. If you'd like to know more about Hygieia Group as a business, it's important to be aware of any risks it's facing. For example, we've found that Hygieia Group has 5 warning signs (1 is concerning!) that deserve your attention before going any further with your analysis.

Our examination of Hygieia Group has focussed on certain factors that can make its earnings look better than they are. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Hygieia Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1650

Hygieia Group

An investment holding company, engages in the provision of general cleaning services in Singapore and Thailand.

Excellent balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor