Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:1172

Magnus Concordia Group (HKG:1172) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Magnus Concordia Group Limited (HKG:1172) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Magnus Concordia Group

What Is Magnus Concordia Group's Debt?

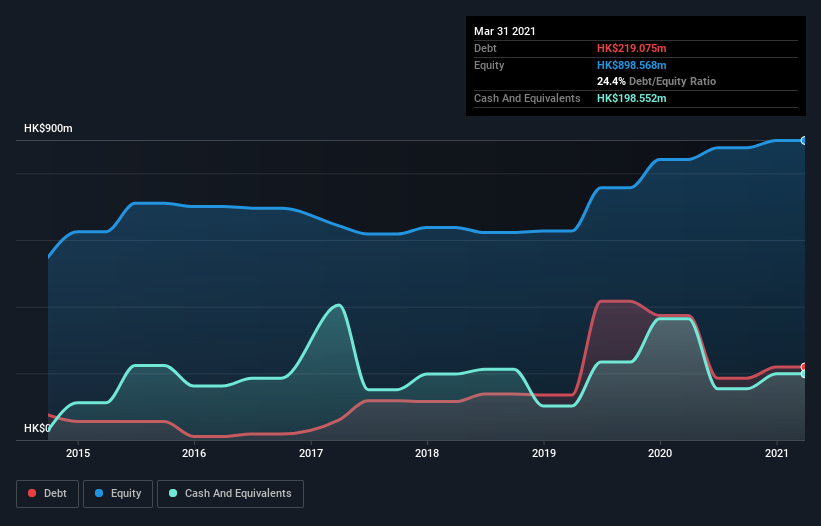

The image below, which you can click on for greater detail, shows that Magnus Concordia Group had debt of HK$219.1m at the end of March 2021, a reduction from HK$373.1m over a year. However, it also had HK$198.6m in cash, and so its net debt is HK$20.5m.

How Healthy Is Magnus Concordia Group's Balance Sheet?

We can see from the most recent balance sheet that Magnus Concordia Group had liabilities of HK$1.86b falling due within a year, and liabilities of HK$336.6m due beyond that. On the other hand, it had cash of HK$198.6m and HK$88.6m worth of receivables due within a year. So its liabilities total HK$1.91b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the HK$381.4m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Magnus Concordia Group would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Magnus Concordia Group has a low net debt to EBITDA ratio of only 0.70. And its EBIT easily covers its interest expense, being 16.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Although Magnus Concordia Group made a loss at the EBIT level, last year, it was also good to see that it generated HK$21m in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Magnus Concordia Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, Magnus Concordia Group actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

We feel some trepidation about Magnus Concordia Group's difficulty level of total liabilities, but we've got positives to focus on, too. For example, its interest cover and conversion of EBIT to free cash flow give us some confidence in its ability to manage its debt. Looking at all the angles mentioned above, it does seem to us that Magnus Concordia Group is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Magnus Concordia Group has 3 warning signs (and 1 which can't be ignored) we think you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1172

Magnus Concordia Group

An investment holding company, engages in the property, printing, and treasury businesses in Hong Kong, Mainland China, the United States, the United Kingdom, France, and internationally.

Low and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor