Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Great Water Holdings Limited (HKG:8196) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Great Water Holdings

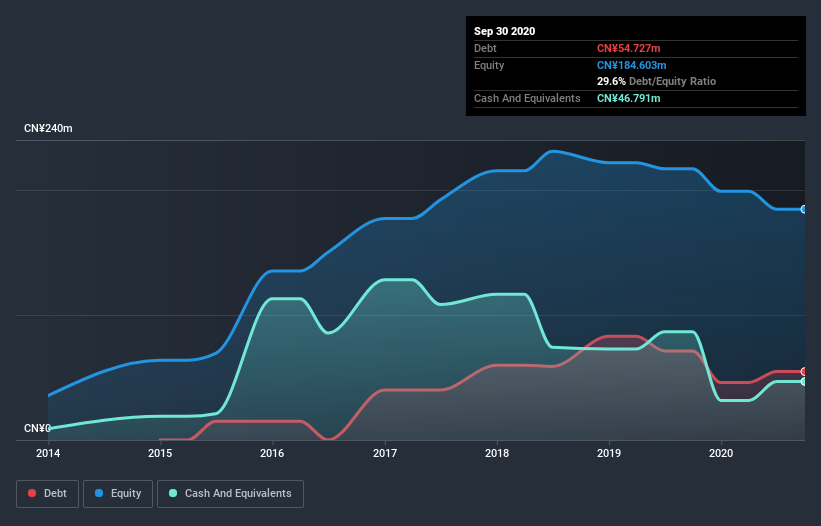

What Is Great Water Holdings's Debt?

The image below, which you can click on for greater detail, shows that Great Water Holdings had debt of CN¥54.7m at the end of June 2020, a reduction from CN¥71.3m over a year. However, it also had CN¥46.8m in cash, and so its net debt is CN¥7.89m.

A Look At Great Water Holdings's Liabilities

Zooming in on the latest balance sheet data, we can see that Great Water Holdings had liabilities of CN¥239.5m due within 12 months and liabilities of CN¥2.04m due beyond that. Offsetting these obligations, it had cash of CN¥46.8m as well as receivables valued at CN¥275.0m due within 12 months. So it actually has CN¥80.2m more liquid assets than total liabilities.

This surplus liquidity suggests that Great Water Holdings's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Great Water Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Great Water Holdings reported revenue of CN¥134m, which is a gain of 85%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

Despite the top line growth, Great Water Holdings still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable CN¥40m at the EBIT level. Having said that, the balance sheet has plenty of liquid assets for now. That will give the company some time and space to grow and develop its business as need be. The company is risky because it will grow into the future to get to profitability and free cash flow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Great Water Holdings (including 1 which is is a bit concerning) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Great Water Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:8196

Futian Holdings

An investment holding company, engages in the provision of engineering services for wastewater and drinking water treatment facilities in Mainland China and Vietnam.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor