Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:8196

Does Great Water Holdings (HKG:8196) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Great Water Holdings Limited (HKG:8196) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Great Water Holdings

What Is Great Water Holdings's Debt?

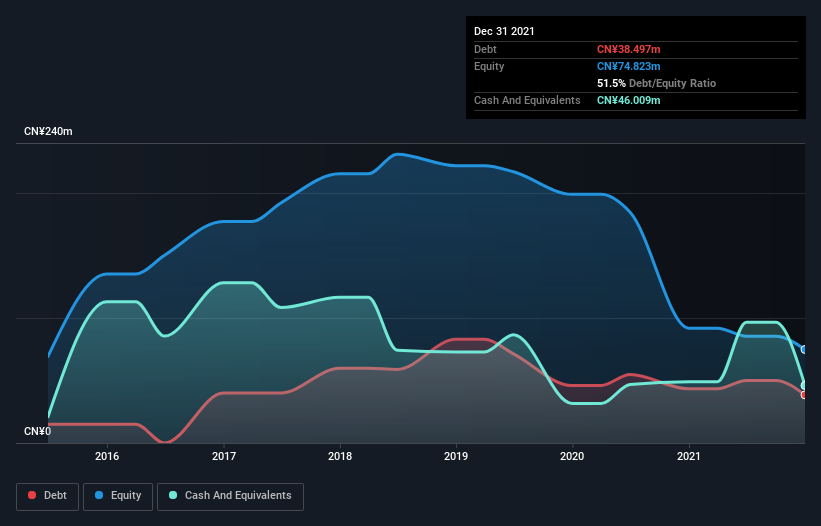

As you can see below, Great Water Holdings had CN¥38.5m of debt at December 2021, down from CN¥43.3m a year prior. But it also has CN¥46.0m in cash to offset that, meaning it has CN¥7.51m net cash.

A Look At Great Water Holdings' Liabilities

According to the last reported balance sheet, Great Water Holdings had liabilities of CN¥264.8m due within 12 months, and liabilities of CN¥4.96m due beyond 12 months. Offsetting this, it had CN¥46.0m in cash and CN¥171.9m in receivables that were due within 12 months. So its liabilities total CN¥51.9m more than the combination of its cash and short-term receivables.

Great Water Holdings has a market capitalization of CN¥249.5m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Great Water Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Great Water Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Great Water Holdings reported revenue of CN¥118m, which is a gain of 57%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Great Water Holdings?

Although Great Water Holdings had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of CN¥8.2m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. One positive is that Great Water Holdings is growing revenue apace, which makes it easier to sell a growth story and raise capital if need be. But that doesn't change our opinion that the stock is risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for Great Water Holdings (1 can't be ignored!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8196

Futian Holdings

An investment holding company, engages in the provision of engineering services for wastewater and drinking water treatment facilities in Mainland China and Vietnam.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor