Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:599

E. Bon Holdings' (HKG:599) Shareholders Will Receive A Bigger Dividend Than Last Year

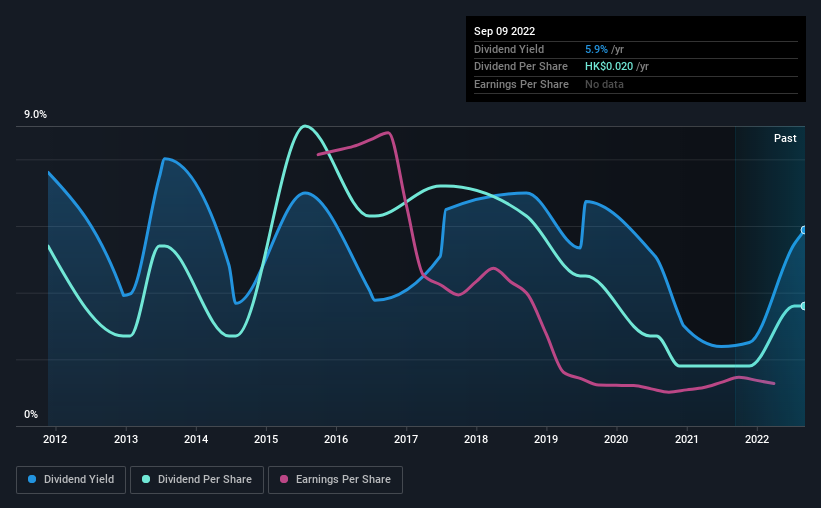

E. Bon Holdings Limited's (HKG:599) dividend will be increasing from last year's payment of the same period to HK$0.01 on 12th of October. Even though the dividend went up, the yield is still quite low at only 5.9%.

See our latest analysis for E. Bon Holdings

E. Bon Holdings' Payment Has Solid Earnings Coverage

Even a low dividend yield can be attractive if it is sustained for years on end. The last payment made up 76% of earnings, but cash flows were much higher. This leaves plenty of cash for reinvestment into the business.

If the company can't turn things around, EPS could fall by 22.4% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could reach 76%, which is definitely on the higher side.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The dividend has gone from an annual total of HK$0.03 in 2012 to the most recent total annual payment of HK$0.02. This works out to be a decline of approximately 4.0% per year over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Over the past five years, it looks as though E. Bon Holdings' EPS has declined at around 22% a year. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future.

In Summary

Overall, we always like to see the dividend being raised, but we don't think E. Bon Holdings will make a great income stock. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 3 warning signs for E. Bon Holdings (1 is significant!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if E. Bon Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:599

E. Bon Holdings

An investment holding company, engages in the importing, wholesale, retail and installation of architectural builders’ hardware, bathroom, kitchen collections, and furniture in the Hong Kong and the People’s Republic of China.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor