What You Can Learn From Sinotruk (Hong Kong) Limited's (HKG:3808) P/E

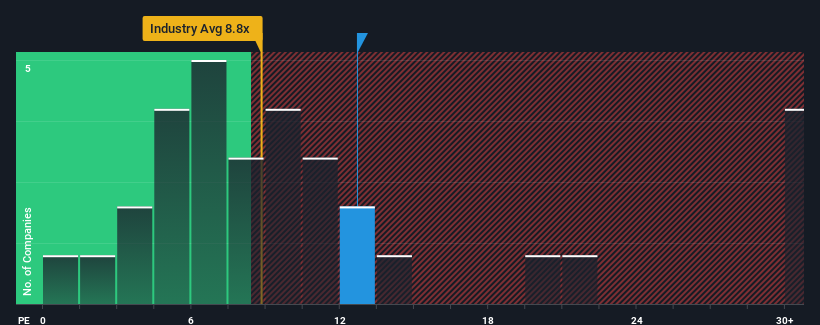

When close to half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") below 9x, you may consider Sinotruk (Hong Kong) Limited (HKG:3808) as a stock to potentially avoid with its 12.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Sinotruk (Hong Kong) certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for Sinotruk (Hong Kong)

How Is Sinotruk (Hong Kong)'s Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Sinotruk (Hong Kong)'s is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 46% gain to the company's bottom line. Still, incredibly EPS has fallen 26% in total from three years ago, which is quite disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 26% each year during the coming three years according to the twelve analysts following the company. That's shaping up to be materially higher than the 16% per annum growth forecast for the broader market.

With this information, we can see why Sinotruk (Hong Kong) is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Sinotruk (Hong Kong)'s P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Sinotruk (Hong Kong) maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Sinotruk (Hong Kong) with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3808

Sinotruk (Hong Kong)

An investment holding company, engages in the research, development, manufacture, and sale of heavy-duty trucks (HDT), medium-heavy duty trucks, light duty trucks (LDT), buses, and related parts and components in Mainland China and internationally.

Excellent balance sheet with proven track record and pays a dividend.