Sinotruk (Hong Kong) (HKG:3808) Is Reducing Its Dividend To CN¥0.33

Sinotruk (Hong Kong) Limited (HKG:3808) is reducing its dividend from last year's comparable payment to CN¥0.33 on the 8th of September. This means that the annual payment will be 2.2% of the current stock price, which is in line with the average for the industry.

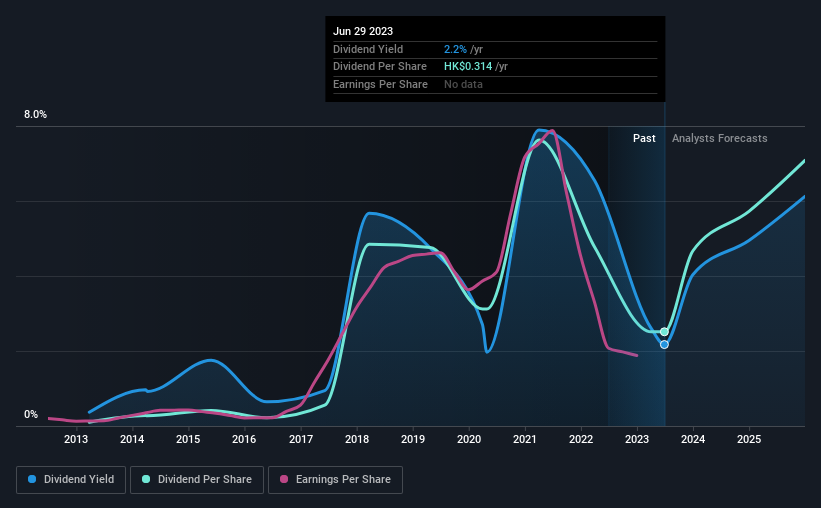

See our latest analysis for Sinotruk (Hong Kong)

Sinotruk (Hong Kong)'s Earnings Easily Cover The Distributions

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. The last dividend was quite easily covered by Sinotruk (Hong Kong)'s earnings. This indicates that quite a large proportion of earnings is being invested back into the business.

Analysts expect a massive rise in earnings per share in the next year. Assuming the dividend continues along recent trends, we think the payout ratio will be 20%, which makes us pretty comfortable with the sustainability of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2013, the dividend has gone from CN¥0.0117 total annually to CN¥0.29. This implies that the company grew its distributions at a yearly rate of about 38% over that duration. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

Dividend Growth Is Doubtful

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. In the last five years, Sinotruk (Hong Kong)'s earnings per share has shrunk at approximately 9.9% per annum. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

In Summary

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We don't think Sinotruk (Hong Kong) is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 1 warning sign for Sinotruk (Hong Kong) that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3808

Sinotruk (Hong Kong)

An investment holding company, engages in the research, development, manufacture, and sale of heavy-duty trucks (HDT), medium-heavy duty trucks, light duty trucks (LDT), buses, and related parts and components in Mainland China and internationally.

Excellent balance sheet with proven track record and pays a dividend.