It is not every day that COSCO SHIPPING Development (SEHK:2866) catches the eye of investors for dramatic reasons. There is no major event or blockbuster headline driving the latest move in the shares. That in itself has some investors wondering if this is a quiet yet meaningful signal, or just everyday noise.

Looking at the numbers, the company’s shares have gradually built up momentum. Over the past year, the stock has delivered a 49% total return, outpacing much of the sector, and gained nearly 17% year-to-date. While short-term price action has been less dramatic, the overall trend points upward, suggesting that expectations around growth or risk might be shifting after a period of subdued trading.

With such steady appreciation, it is fair to ask whether COSCO SHIPPING Development is undervalued at this level or if the market is already factoring in every ounce of future growth.

Advertisement

Price-to-Earnings of 8.2x: Is it justified?

COSCO SHIPPING Development is currently valued at a price-to-earnings (P/E) ratio of 8.2x, which is below both its industry peers and the broader Hong Kong market. This suggests the stock could be attractively priced compared to similar companies and the overall market context.

The price-to-earnings multiple measures what investors are willing to pay today for a company’s historical or projected earnings. In the capital goods and trade distribution sector, this ratio is a useful benchmark because it highlights whether the market is optimistic or cautious about future profitability and growth potential compared to peers.

Peers in the Hong Kong Trade Distributors industry currently trade at an average P/E of 10.4x. The Hong Kong market average is 12.2x. With COSCO SHIPPING Development’s multiple well below both, investors may be pricing in slower growth or higher perceived risk, or potentially overlooking positive earnings momentum. Overall, its lower P/E could indicate underappreciated value if current earnings trends persist.

However, shifting outlooks on global trade or unexpected changes in earnings could quickly challenge this positive momentum for COSCO SHIPPING Development.

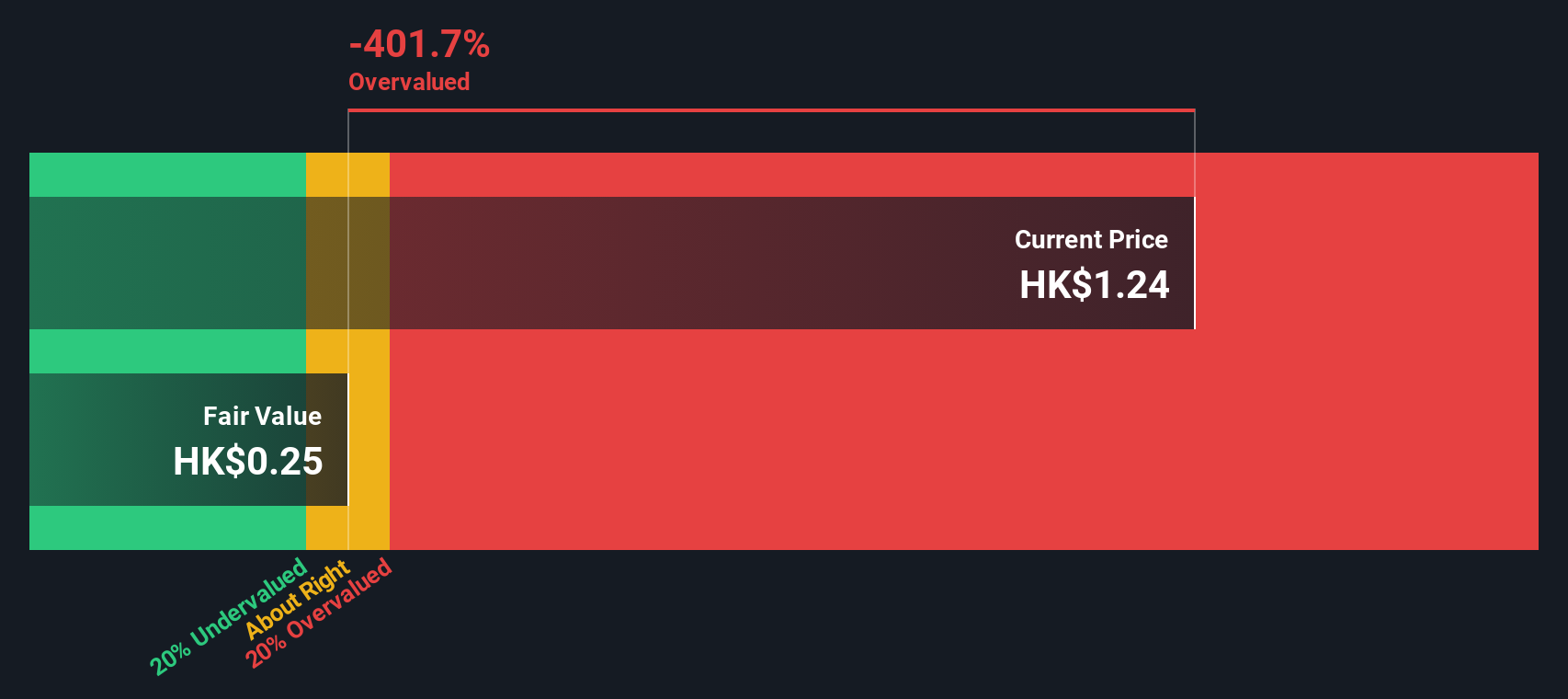

While valuation based on earnings appears favorable, our SWS DCF model tells a very different story. This method suggests the stock may actually be overvalued, which calls into question how reliable these traditional benchmarks really are. Could fundamentals or optimism be winning out?

Build Your Own COSCO SHIPPING Development Narrative

If you see things differently, or want to dig deeper for yourself, you can easily build your own narrative and reach a conclusion in just a few minutes. Do it your way

A great starting point for your COSCO SHIPPING Development research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock even more investing opportunities with Simply Wall Street’s screeners. If you hesitate, you could miss trending stocks and untapped growth the market rarely hands out twice.

Secure your portfolio with income potential by targeting companies offering dividend stocks with yields > 3% and yields that outshine savings accounts.

Get ahead of the next tech breakthrough by backing pioneers in supercomputing. Start with quantum computing stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.