- Hong Kong

- /

- Electrical

- /

- SEHK:2727

Shanghai Electric Group (HKG:2727) Will Be Hoping To Turn Its Returns On Capital Around

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after investigating Shanghai Electric Group (HKG:2727), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Shanghai Electric Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0088 = CN¥1.0b ÷ (CN¥287b - CN¥168b) (Based on the trailing twelve months to September 2023).

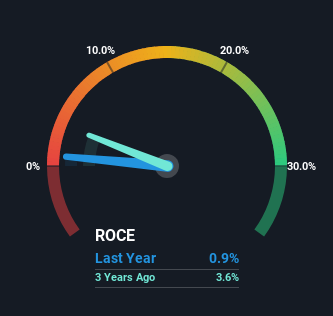

Thus, Shanghai Electric Group has an ROCE of 0.9%. In absolute terms, that's a low return and it also under-performs the Electrical industry average of 5.3%.

See our latest analysis for Shanghai Electric Group

Above you can see how the current ROCE for Shanghai Electric Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Shanghai Electric Group .

How Are Returns Trending?

When we looked at the ROCE trend at Shanghai Electric Group, we didn't gain much confidence. Over the last five years, returns on capital have decreased to 0.9% from 3.2% five years ago. On the other hand, the company has been employing more capital without a corresponding improvement in sales in the last year, which could suggest these investments are longer term plays. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a side note, Shanghai Electric Group's current liabilities are still rather high at 59% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

The Bottom Line

Bringing it all together, while we're somewhat encouraged by Shanghai Electric Group's reinvestment in its own business, we're aware that returns are shrinking. And in the last five years, the stock has given away 46% so the market doesn't look too hopeful on these trends strengthening any time soon. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

Shanghai Electric Group could be trading at an attractive price in other respects, so you might find our free intrinsic value estimation for 2727 on our platform quite valuable.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2727

Shanghai Electric Group

Provides industrial-grade eco-friendly smart system solutions in Mainland China and internationally.

Undervalued with excellent balance sheet.