Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:223

Elife Holdings Limited's (HKG:223) CEO Compensation Looks Acceptable To Us And Here's Why

Performance at Elife Holdings Limited (HKG:223) has been rather uninspiring recently and shareholders may be wondering how CEO Sui Keung Chiu plans to fix this. They will get a chance to exercise their voting power to influence the future direction of the company in the next AGM on 29 September 2022. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for Elife Holdings

Comparing Elife Holdings Limited's CEO Compensation With The Industry

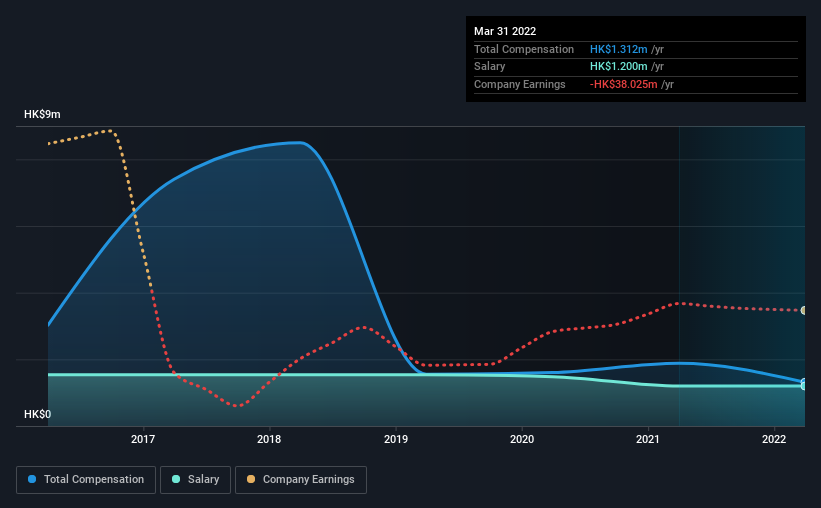

At the time of writing, our data shows that Elife Holdings Limited has a market capitalization of HK$96m, and reported total annual CEO compensation of HK$1.3m for the year to March 2022. Notably, that's a decrease of 30% over the year before. We note that the salary portion, which stands at HK$1.20m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$2.7m. This suggests that Sui Keung Chiu is paid below the industry median. Moreover, Sui Keung Chiu also holds HK$724k worth of Elife Holdings stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | HK$1.2m | HK$1.2m | 91% |

| Other | HK$112k | HK$681k | 9% |

| Total Compensation | HK$1.3m | HK$1.9m | 100% |

On an industry level, roughly 75% of total compensation represents salary and 25% is other remuneration. Elife Holdings pays out 91% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Elife Holdings Limited's Growth

Elife Holdings Limited's earnings per share (EPS) grew 71% per year over the last three years. In the last year, its revenue is down 45%.

This demonstrates that the company has been improving recently and is good news for the shareholders. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Elife Holdings Limited Been A Good Investment?

Few Elife Holdings Limited shareholders would feel satisfied with the return of -79% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

The loss to shareholders over the past three years is certainly concerning. The share price trend has diverged with the robust growth in EPS however, suggesting there may be other factors that could be driving the price performance. A key focus for the board and management will be how to align the share price with fundamentals. In the upcoming AGM, shareholders will get the opportunity to discuss these concerns with the board and assess if the board's plan is likely to improve company performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We did our research and identified 4 warning signs (and 1 which is significant) in Elife Holdings we think you should know about.

Switching gears from Elife Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Elife Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:223

Elife Holdings

An investment holding company, engages in the supply chain business for branded goods and consumer products in Hong Kong and the People’s Republic of China.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor