- Hong Kong

- /

- Trade Distributors

- /

- SEHK:2102

Tak Lee Machinery Holdings' (HKG:2102) Anemic Earnings Might Be Worse Than You Think

The subdued market reaction suggests that Tak Lee Machinery Holdings Limited's (HKG:2102) recent earnings didn't contain any surprises. Our analysis suggests that along with soft profit numbers, investors should be aware of some other underlying weaknesses in the numbers.

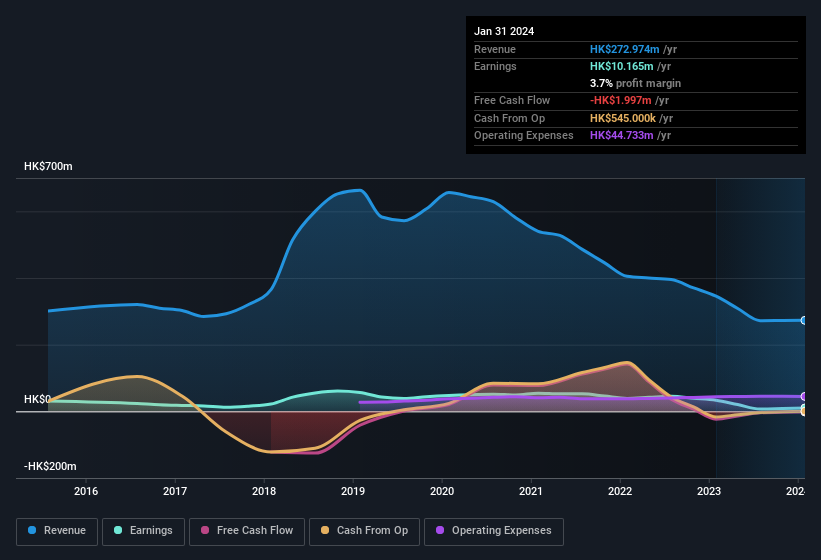

Check out our latest analysis for Tak Lee Machinery Holdings

The Impact Of Unusual Items On Profit

For anyone who wants to understand Tak Lee Machinery Holdings' profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from HK$2.0m worth of unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And that's as you'd expect, given these boosts are described as 'unusual'. If Tak Lee Machinery Holdings doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Tak Lee Machinery Holdings.

Our Take On Tak Lee Machinery Holdings' Profit Performance

We'd posit that Tak Lee Machinery Holdings' statutory earnings aren't a clean read on ongoing productivity, due to the large unusual item. Therefore, it seems possible to us that Tak Lee Machinery Holdings' true underlying earnings power is actually less than its statutory profit. Sadly, its EPS was down over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you'd like to know more about Tak Lee Machinery Holdings as a business, it's important to be aware of any risks it's facing. Our analysis shows 4 warning signs for Tak Lee Machinery Holdings (1 is concerning!) and we strongly recommend you look at these before investing.

This note has only looked at a single factor that sheds light on the nature of Tak Lee Machinery Holdings' profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking to trade Tak Lee Machinery Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tak Lee Machinery Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2102

Tak Lee Machinery Holdings

An investment holding company, engages in the sale and leasing of new and used earthmoving equipment and spare parts in Hong Kong.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives