- Hong Kong

- /

- Construction

- /

- SEHK:1987

Investors Appear Satisfied With Beng Soon Machinery Holdings Limited's (HKG:1987) Prospects As Shares Rocket 33%

Despite an already strong run, Beng Soon Machinery Holdings Limited (HKG:1987) shares have been powering on, with a gain of 33% in the last thirty days. Taking a wider view, although not as strong as the last month, the full year gain of 16% is also fairly reasonable.

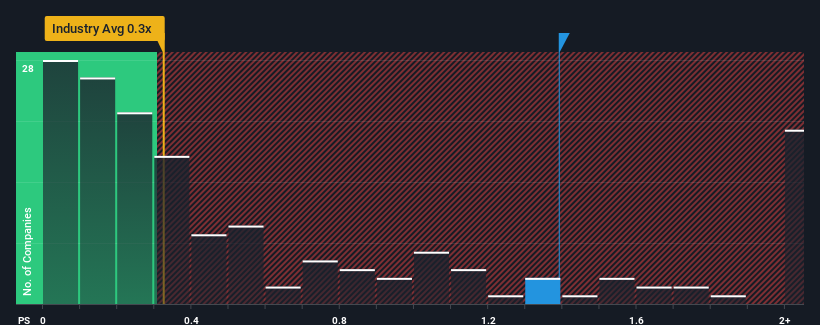

After such a large jump in price, you could be forgiven for thinking Beng Soon Machinery Holdings is a stock not worth researching with a price-to-sales ratios (or "P/S") of 1.4x, considering almost half the companies in Hong Kong's Construction industry have P/S ratios below 0.3x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Beng Soon Machinery Holdings

How Beng Soon Machinery Holdings Has Been Performing

For instance, Beng Soon Machinery Holdings' receding revenue in recent times would have to be some food for thought. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. If not, then existing shareholders may be quite nervous about the viability of the share price.

Although there are no analyst estimates available for Beng Soon Machinery Holdings, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Beng Soon Machinery Holdings' Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Beng Soon Machinery Holdings' to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 10%. Even so, admirably revenue has lifted 198% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

This is in contrast to the rest of the industry, which is expected to grow by 9.5% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this in consideration, it's not hard to understand why Beng Soon Machinery Holdings' P/S is high relative to its industry peers. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

The large bounce in Beng Soon Machinery Holdings' shares has lifted the company's P/S handsomely. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Beng Soon Machinery Holdings revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

Before you take the next step, you should know about the 4 warning signs for Beng Soon Machinery Holdings that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Beng Soon Machinery Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1987

Beng Soon Machinery Holdings

Beng Soon Machinery Holdings Limited, investment holding company, provides demolition services to public and private sector clients in Singapore.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives