Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1891

We Think Heng Hup Holdings (HKG:1891) Has A Fair Chunk Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Heng Hup Holdings Limited (HKG:1891) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Heng Hup Holdings

What Is Heng Hup Holdings's Net Debt?

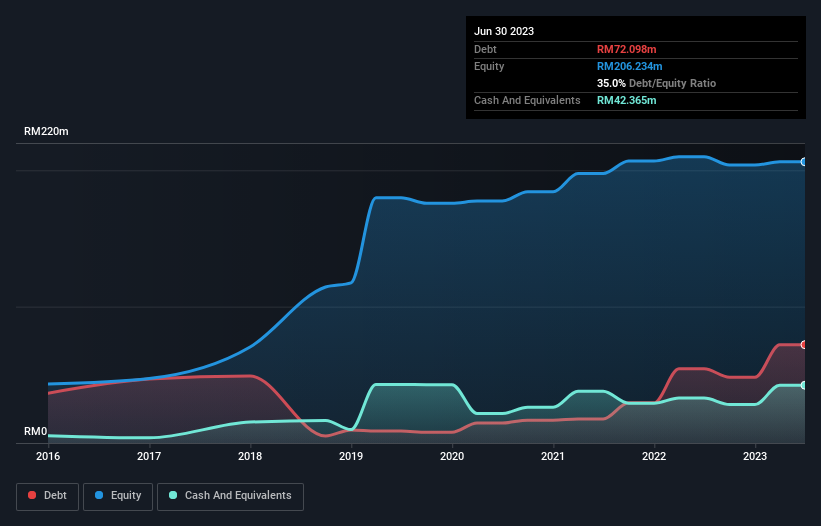

As you can see below, at the end of June 2023, Heng Hup Holdings had RM72.1m of debt, up from RM54.4m a year ago. Click the image for more detail. However, because it has a cash reserve of RM42.4m, its net debt is less, at about RM29.7m.

How Healthy Is Heng Hup Holdings' Balance Sheet?

We can see from the most recent balance sheet that Heng Hup Holdings had liabilities of RM89.9m falling due within a year, and liabilities of RM19.0m due beyond that. Offsetting these obligations, it had cash of RM42.4m as well as receivables valued at RM139.3m due within 12 months. So it can boast RM72.8m more liquid assets than total liabilities.

This surplus liquidity suggests that Heng Hup Holdings' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. When analysing debt levels, the balance sheet is the obvious place to start. But it is Heng Hup Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Heng Hup Holdings made a loss at the EBIT level, and saw its revenue drop to RM1.1b, which is a fall of 27%. That makes us nervous, to say the least.

Caveat Emptor

Not only did Heng Hup Holdings's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost RM788k at the EBIT level. Having said that, the balance sheet has plenty of liquid assets for now. That should give the business time to grow its cashflow. While the stock is probably a bit risky, there may be an opportunity if the business itself improves, allowing the company to stage a recovery. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Heng Hup Holdings (of which 1 doesn't sit too well with us!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Heng Hup Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1891

Heng Hup Holdings

An investment holding company, engages in the trading of scrap ferrous metal in Malaysia.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor