The board of Wecon Holdings Limited (HKG:1793) has announced that it will pay a dividend on the 19th of September, with investors receiving HK$0.012 per share. This payment means that the dividend yield will be 6.0%, which is around the industry average.

View our latest analysis for Wecon Holdings

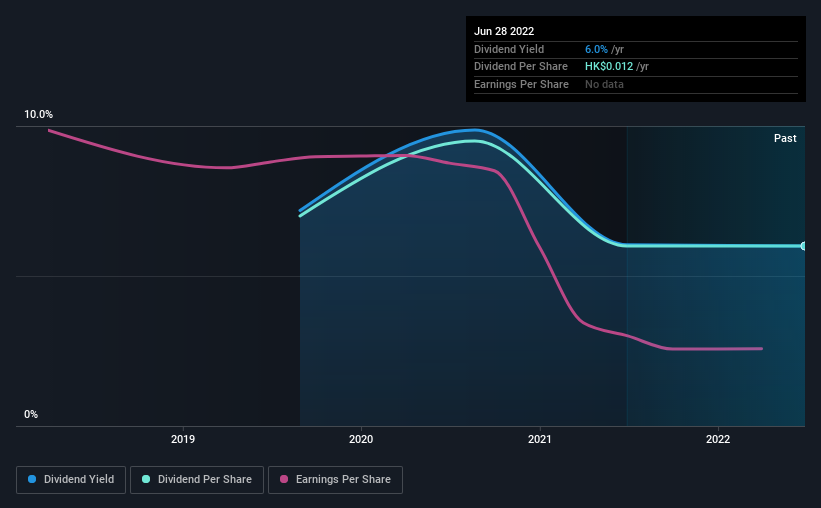

Wecon Holdings Doesn't Earn Enough To Cover Its Payments

Unless the payments are sustainable, the dividend yield doesn't mean too much. Prior to this announcement, Wecon Holdings' earnings easily covered the dividend, but free cash flows were negative. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

Looking forward, EPS could fall by 33.4% if the company can't turn things around from the last few years. If the dividend continues along the path it has been on recently, the payout ratio in 12 months could be 102%, which is definitely a bit high to be sustainable going forward.

Wecon Holdings' Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. Since 2019, the first annual payment was HK$0.014, compared to the most recent full-year payment of HK$0.012. Doing the maths, this is a decline of about 5.0% per year. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Has Limited Growth Potential

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Earnings per share has been sinking by 33% over the last three years. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future.

The Dividend Could Prove To Be Unreliable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While the low payout ratio is redeeming feature, this is offset by the minimal cash to cover the payments. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 3 warning signs for Wecon Holdings (1 makes us a bit uncomfortable!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Wecon Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1793

Wecon Holdings

An investment holding company, operates as a construction contractor in Hong Kong.

Flawless balance sheet slight.

Market Insights

Community Narratives