Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1539

This Is The Reason Why We Think Unity Group Holdings International Limited's (HKG:1539) CEO Might Be Underpaid

Key Insights

- Unity Group Holdings International's Annual General Meeting to take place on 28th of September

- Salary of HK$1.43m is part of CEO Mansfield Wong's total remuneration

- The overall pay is 51% below the industry average

- Unity Group Holdings International's EPS grew by 33% over the past three years while total shareholder return over the past three years was 243%

The impressive results at Unity Group Holdings International Limited (HKG:1539) recently will be great news for shareholders. At the upcoming AGM on 28th of September, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. We think the CEO has done a pretty decent job and probably deserves a well-earned pay rise.

Check out our latest analysis for Unity Group Holdings International

Comparing Unity Group Holdings International Limited's CEO Compensation With The Industry

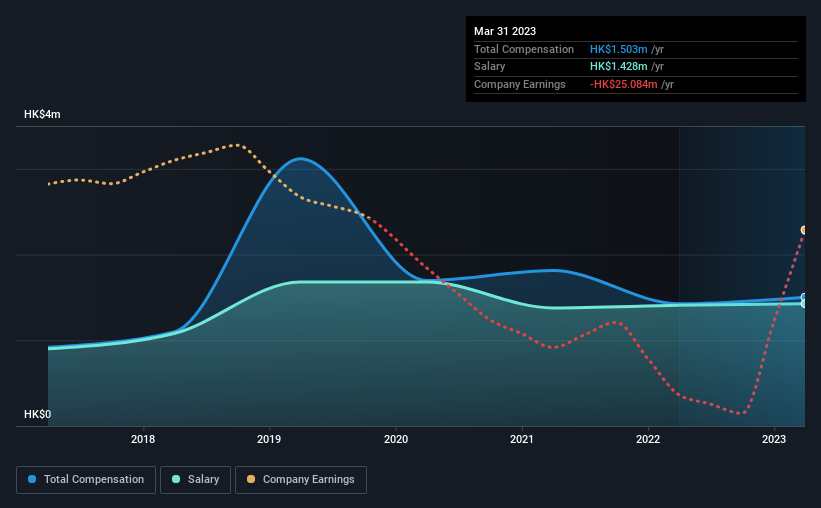

According to our data, Unity Group Holdings International Limited has a market capitalization of HK$1.5b, and paid its CEO total annual compensation worth HK$1.5m over the year to March 2023. That's just a smallish increase of 5.4% on last year. We note that the salary portion, which stands at HK$1.43m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Hong Kong Trade Distributors industry with market capitalizations ranging from HK$782m to HK$3.1b, the reported median CEO total compensation was HK$3.1m. In other words, Unity Group Holdings International pays its CEO lower than the industry median. Furthermore, Mansfield Wong directly owns HK$906m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$1.4m | HK$1.4m | 95% |

| Other | HK$75k | HK$18k | 5% |

| Total Compensation | HK$1.5m | HK$1.4m | 100% |

On an industry level, around 93% of total compensation represents salary and 7% is other remuneration. Investors will find it interesting that Unity Group Holdings International pays the bulk of its rewards through a traditional salary, instead of non-salary benefits. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Unity Group Holdings International Limited's Growth Numbers

Unity Group Holdings International Limited's earnings per share (EPS) grew 33% per year over the last three years. Its revenue is down 42% over the previous year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Unity Group Holdings International Limited Been A Good Investment?

Boasting a total shareholder return of 243% over three years, Unity Group Holdings International Limited has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Mansfield receives almost all of their compensation through a salary. Some shareholders will probably be more lenient on CEO compensation in the upcoming AGM given the pleasing performance of the company recently. However, despite the strong growth in earnings and share price growth, the focus for shareholders would be how the company plans to steer the company towards sustainable profitability in the near future.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We identified 2 warning signs for Unity Group Holdings International (1 is significant!) that you should be aware of before investing here.

Switching gears from Unity Group Holdings International, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1539

Unity Group Holdings International

An investment holding company, engages in the leasing and trading of energy saving products.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor