Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1539

Investors Appear Satisfied With Unity Group Holdings International Limited's (HKG:1539) Prospects As Shares Rocket 25%

Unity Group Holdings International Limited (HKG:1539) shareholders would be excited to see that the share price has had a great month, posting a 25% gain and recovering from prior weakness. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 6.0% in the last twelve months.

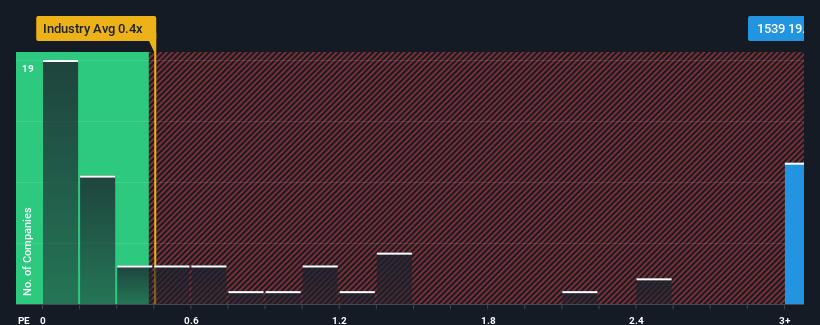

Following the firm bounce in price, you could be forgiven for thinking Unity Group Holdings International is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 19.8x, considering almost half the companies in Hong Kong's Trade Distributors industry have P/S ratios below 0.4x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Unity Group Holdings International

How Has Unity Group Holdings International Performed Recently?

With revenue growth that's superior to most other companies of late, Unity Group Holdings International has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Unity Group Holdings International.What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as steep as Unity Group Holdings International's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company grew revenue by an impressive 72% last year. The latest three year period has also seen an excellent 183% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 115% during the coming year according to the one analyst following the company. That's shaping up to be materially higher than the 34% growth forecast for the broader industry.

With this information, we can see why Unity Group Holdings International is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Unity Group Holdings International's P/S?

Shares in Unity Group Holdings International have seen a strong upwards swing lately, which has really helped boost its P/S figure. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Unity Group Holdings International maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Trade Distributors industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Unity Group Holdings International is showing 3 warning signs in our investment analysis, and 2 of those shouldn't be ignored.

If you're unsure about the strength of Unity Group Holdings International's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1539

Unity Group Holdings International

An investment holding company, engages in the leasing and trading of energy saving products.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor