Advertisement

There Could Be A Chance Zhejiang Tengy Environmental Technology Co., Ltd's (HKG:1527) CEO Will Have Their Compensation Increased

Key Insights

- Zhejiang Tengy Environmental Technology to hold its Annual General Meeting on 30th of May

- Salary of CN¥447.0k is part of CEO Tianjie Bian's total remuneration

- Total compensation is 73% below industry average

- Zhejiang Tengy Environmental Technology's EPS grew by 60% over the past three years while total shareholder return over the past three years was 8.8%

Shareholders will be pleased by the robust performance of Zhejiang Tengy Environmental Technology Co., Ltd (HKG:1527) recently and this will be kept in mind in the upcoming AGM on 30th of May. The focus will probably be on the future strategic initiatives that the board and management will put in place to improve the business rather than executive remuneration when they cast their votes on company resolutions. We have prepared some analysis below and we show why we think CEO compensation looks decent with even the possibility for a raise.

Check out our latest analysis for Zhejiang Tengy Environmental Technology

Comparing Zhejiang Tengy Environmental Technology Co., Ltd's CEO Compensation With The Industry

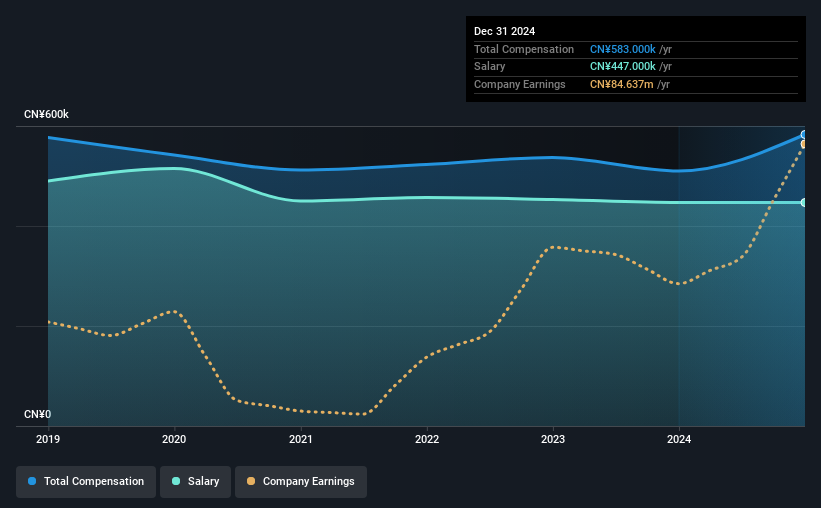

Our data indicates that Zhejiang Tengy Environmental Technology Co., Ltd has a market capitalization of HK$181m, and total annual CEO compensation was reported as CN¥583k for the year to December 2024. That's a notable increase of 14% on last year. Notably, the salary which is CN¥447.0k, represents most of the total compensation being paid.

In comparison with other companies in the Hong Kong Machinery industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was CN¥2.1m. That is to say, Tianjie Bian is paid under the industry median. Furthermore, Tianjie Bian directly owns HK$10m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥447k | CN¥447k | 77% |

| Other | CN¥136k | CN¥63k | 23% |

| Total Compensation | CN¥583k | CN¥510k | 100% |

On an industry level, around 77% of total compensation represents salary and 23% is other remuneration. Although there is a difference in how total compensation is set, Zhejiang Tengy Environmental Technology more or less reflects the market in terms of setting the salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Zhejiang Tengy Environmental Technology Co., Ltd's Growth

Over the past three years, Zhejiang Tengy Environmental Technology Co., Ltd has seen its earnings per share (EPS) grow by 60% per year. In the last year, its revenue is up 20%.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Zhejiang Tengy Environmental Technology Co., Ltd Been A Good Investment?

With a total shareholder return of 8.8% over three years, Zhejiang Tengy Environmental Technology Co., Ltd has done okay by shareholders, but there's always room for improvement. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 2 warning signs for Zhejiang Tengy Environmental Technology (of which 1 shouldn't be ignored!) that you should know about in order to have a holistic understanding of the stock.

Important note: Zhejiang Tengy Environmental Technology is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Tengy Environmental Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1527

Zhejiang Tengy Environmental Technology

Designs, develops, manufactures, installs, and sells environmental pollution prevention equipment and electronic products in Mainland China and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor