Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:1499

Some Confidence Is Lacking In OKG Technology Holdings Limited (HKG:1499) As Shares Slide 27%

The OKG Technology Holdings Limited (HKG:1499) share price has fared very poorly over the last month, falling by a substantial 27%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 43% share price drop.

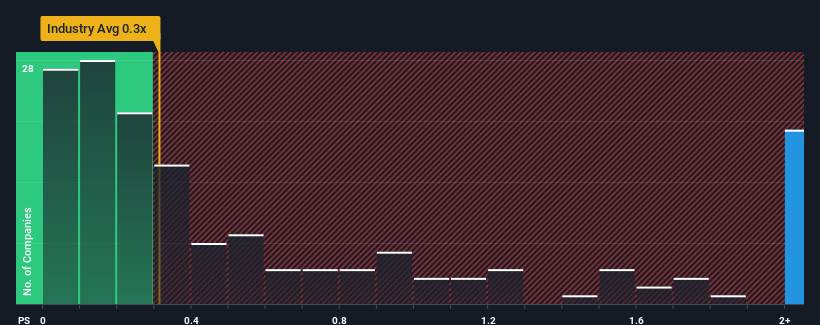

Even after such a large drop in price, you could still be forgiven for thinking OKG Technology Holdings is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 3.6x, considering almost half the companies in Hong Kong's Construction industry have P/S ratios below 0.3x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for OKG Technology Holdings

What Does OKG Technology Holdings' P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at OKG Technology Holdings over the last year, which is not ideal at all. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on OKG Technology Holdings will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For OKG Technology Holdings?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like OKG Technology Holdings' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 21% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 43% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 11% shows it's an unpleasant look.

In light of this, it's alarming that OKG Technology Holdings' P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Final Word

OKG Technology Holdings' shares may have suffered, but its P/S remains high. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of OKG Technology Holdings revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for OKG Technology Holdings with six simple checks.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1499

OKG Technology Holdings

An investment holding company, provides foundation works, building construction works, and ancillary services in the People’s Republic of China and Hong Kong.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor