Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1341

Hao Tian (SEHK:1341) Reports Widening Net Losses, Reinforcing Bearish Narratives on Profitability

Simply Wall St

Reviewed by Simply Wall St

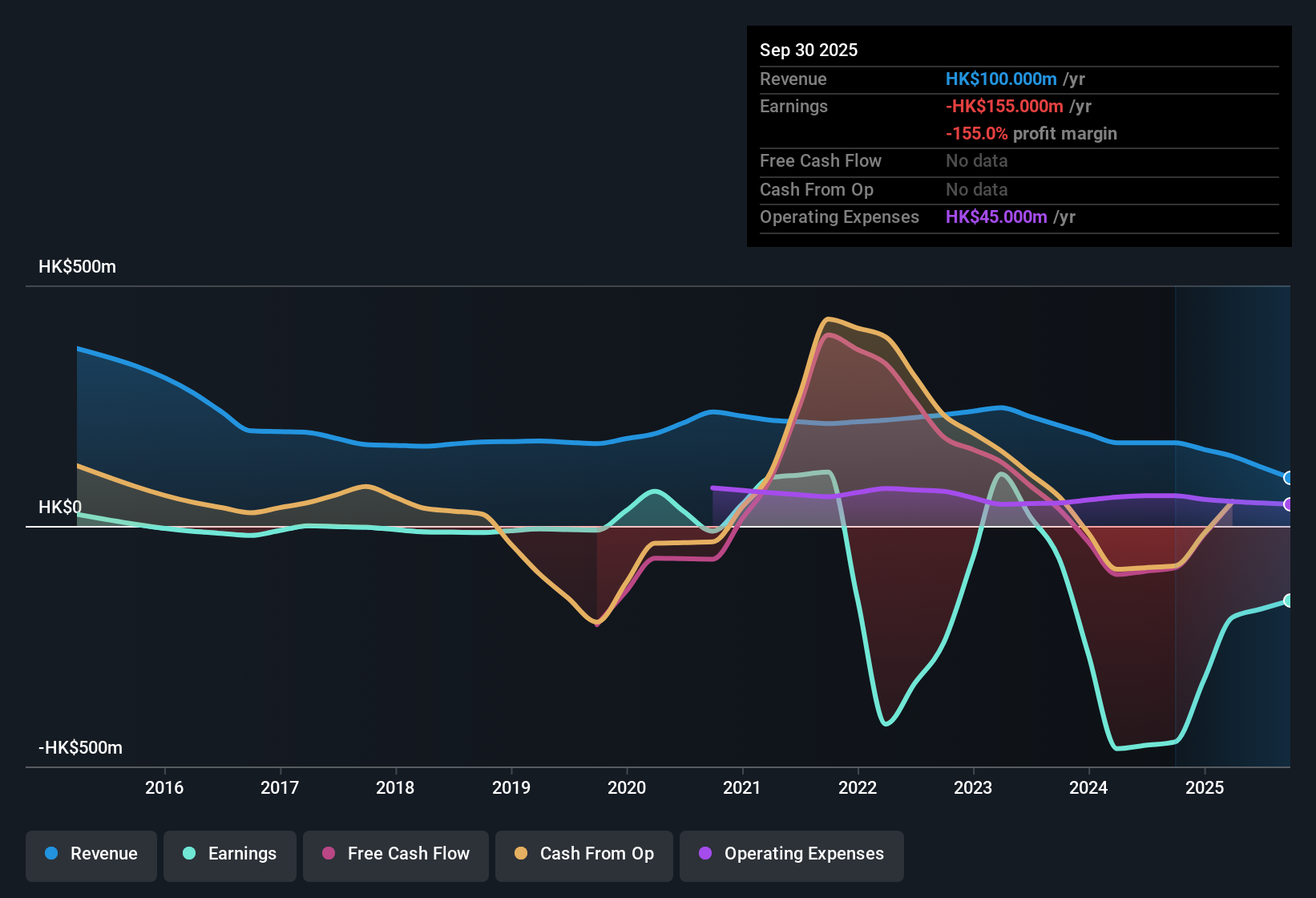

Hao Tian International Construction Investment Group (SEHK:1341) just released its H1 2026 results, posting revenue of 100 million HKD and a basic EPS of -0.019633 HKD in the trailing twelve months. Looking at the last couple of halves, revenue moved from 173 million HKD in H1 2025 to 145 million HKD in H2 2025, with net income staying deep in the red during both periods. Investors face a tough earnings season as margins remain compressed.

See our full analysis for Hao Tian International Construction Investment Group.Now let's see how this latest set of numbers compares with the most widely held narratives. Some might hold up, while others could be challenged by what has just been reported.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Widen as Net Income Drops to Negative 155 Million HKD

- Net income for the trailing twelve months fell to -155 million HKD, deepening from -190 million HKD in H2 2025 and -449 million HKD in H1 2025, with basic EPS remaining negative at -0.019633 HKD.

- Looking at the current market sentiment, what stands out is the lack of any real profit turnaround. The ongoing unprofitability underlines critics’ concerns that operational improvements remain out of reach.

- Bears point out that net losses are consistent and substantial, with no evidence of margin recovery across multiple reporting periods.

- The lack of any profit growth acceleration or notable cost discipline materially supports the bearish case for persistent earnings pressure.

Valuation Premium: Price-to-Sales at 13.4x

- The current price-to-sales ratio sits at 13.4x, which is much higher than the Hong Kong Trade Distributors industry average of 0.6x and the peer average of 8.2x.

- What is surprising is the company’s ability to command such a high sales multiple despite heavy losses. This highlights a tension that market watchers say points to a valuation disconnected from underlying profitability.

- This premium persists even as the share price of HK$0.12 trades above DCF fair value of HK$0.08, underscoring ongoing concerns about overvaluation among risk-focused investors.

- With no positive earnings momentum, skeptics argue it is difficult to justify the steep multiple without a credible path to profits.

Shareholder Dilution and Volatility Intensify Risk

- Shareholders experienced substantial dilution over the past year, adding to already heightened share price volatility compared to the broader Hong Kong market.

- Industry observers note that this combination of dilution and rising volatility strengthens the view that operational and capital structure risks are center stage for investors right now.

- The lack of reward factors reported, alongside persistent unprofitability, signals that risk outweighs potential upside in the current outlook.

- Market narratives increasingly focus on how shareholder dilution has amplified the hurdles for any future turnaround.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Hao Tian International Construction Investment Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Hao Tian International Construction Investment Group continues to face persistent losses, shareholder dilution, and an overstretched valuation without a convincing path to profitability or financial recovery.

If you want to focus on companies trading at more attractive prices relative to their fundamentals, check out these 919 undervalued stocks based on cash flows and spot opportunities where the numbers stack up in your favor.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hao Tian International Construction Investment Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1341

Hao Tian International Construction Investment Group

An investment holding company, operates in the construction machinery business in Hong Kong, the United Kingdom, the People’s Republic of China, Malaysia, Cambodia, and Macau.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative