Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:1183

MECOM Power and Construction (HKG:1183) Is Increasing Its Dividend To HK$0.033

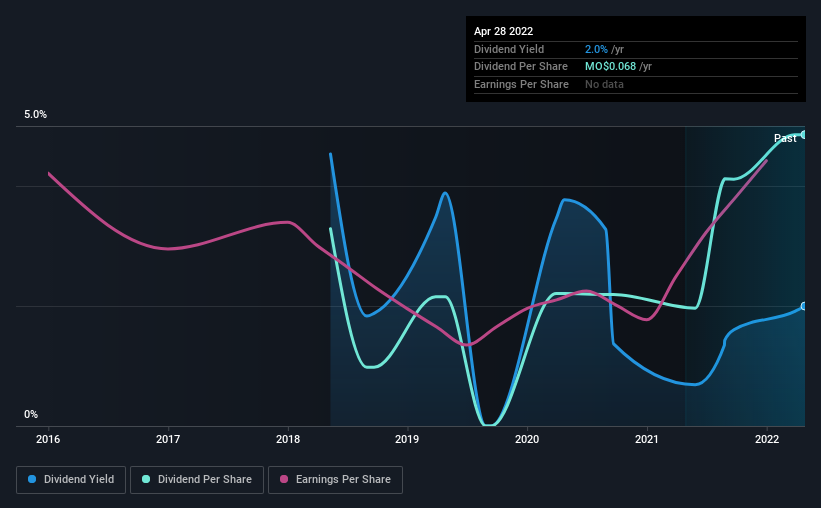

MECOM Power and Construction Limited (HKG:1183) will increase its dividend on the 29th of June to HK$0.033. Despite this raise, the dividend yield of 1.8% is only a modest boost to shareholder returns.

See our latest analysis for MECOM Power and Construction

MECOM Power and Construction's Payment Has Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. The last payment made up 89% of earnings, but cash flows were much higher. This leaves plenty of cash for reinvestment into the business.

EPS is set to grow by 8.5% over the next year if recent trends continue. If the dividend continues growing along recent trends, we estimate the payout ratio could reach 82%, which is on the higher side, but certainly still feasible.

MECOM Power and Construction's Dividend Has Lacked Consistency

The track record isn't the longest, but we are already seeing a bit of instability in the payments. Since 2018, the dividend has gone from MO$0.046 to MO$0.068. This means that it has been growing its distributions at 10% per annum over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Has Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. We are encouraged to see that MECOM Power and Construction has grown earnings per share at 8.5% per year over the past five years. The payout ratio is very much on the higher end, which could mean that the growth rate will slow down in the future, and that could flow through to the dividend as well.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. See if management have their own wealth at stake, by checking insider shareholdings in MECOM Power and Construction stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1183

MECOM Power and Construction

Provides construction services in Macau, Hong Kong, Cyprus, and the People’s Republic of China.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor