Advertisement

- Hong Kong

- /

- Industrials

- /

- SEHK:1

A Look at CK Hutchison Holdings (SEHK:1) Valuation as AS Watson Group IPO Considered

Simply Wall St

Reviewed by Simply Wall St

CK Hutchison Holdings (SEHK:1) is exploring the possibility of listing its health and beauty retail business, AS Watson Group, on the stock market. Early talks suggest that a Hong Kong IPO and potentially a UK listing are under consideration.

See our latest analysis for CK Hutchison Holdings.

After a steady run of positive news, CK Hutchison Holdings’ shares have gathered real momentum, notching a 33.7% share price return since the start of the year and an impressive 43.3% total shareholder return over 12 months. Investors are clearly reacting to recent strategic moves and speculation around the AS Watson listing, which suggests the market sees renewed growth potential ahead.

If the buzz around CK Hutchison has you watching for the next breakout, this could be the perfect moment to broaden your horizons and discover fast growing stocks with high insider ownership

But with shares already up sharply and a potential listing on the horizon, investors may be wondering if CK Hutchison remains undervalued in the market or if the recent rally has already factored in future growth prospects.

Most Popular Narrative: 11.1% Undervalued

With the most widely followed valuation narrative implying a fair value of HK$61.73, well above the recent close of HK$54.90, it is clear the consensus sees further upside potential if recent projections play out. This view hinges on ongoing business transformations and the belief that expansion drives bottom-line gains beyond what the current market price suggests.

Sustained investment and efficiency-driven growth in the Ports division, including expanded facilities in key geographies and increased storage income, position the company to benefit from global trade resilience and supply chain optimization, supporting higher revenue and stable cash flows. Strategic expansion and modernization of the group's retail arm (notably A.S. Watson's store portfolio and loyalty program development, plus omni-channel/dark store initiatives), are anticipated to drive same-store sales growth and operational leverage, contributing to higher revenue and sustainable bottom-line growth.

Curious about the storyline behind this bullish valuation? The narrative hints at ambitious operational upgrades and bold revenue targets, factors that could reshape investor expectations. Don't miss the specifics fueling this projected upside.

Result: Fair Value of $61.73 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifting consumer demand in China and a reliance on non-recurring gains could quickly dampen optimism and place pressure on CK Hutchison’s outlook.

Find out about the key risks to this CK Hutchison Holdings narrative.

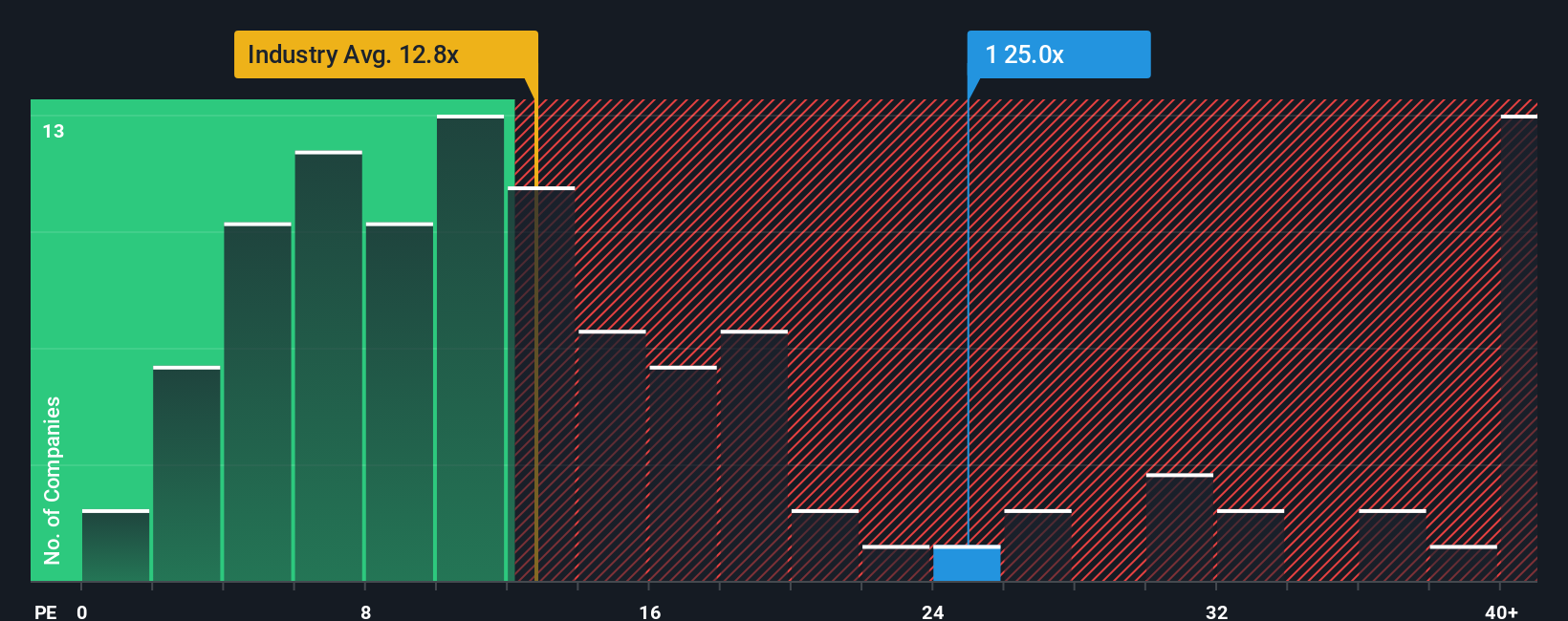

Another View: Market Ratios Send a Caution Signal

While the consensus points to CK Hutchison shares being undervalued, the market’s current price-to-earnings ratio tells a different story. At 27.3x, it is higher than both the peer average (25.3x) and the Asian Industrials industry average (10.9x), and well above its estimated fair ratio of 18.9x. This suggests investors may be paying up for growth that has not yet materialized, raising questions about how much further the stock can climb before value concerns take hold.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CK Hutchison Holdings Narrative

If you have your own perspective or want to go hands-on with the data, you can dive in and craft your own narrative in just a few minutes. Do it your way

A great starting point for your CK Hutchison Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t leave your portfolio on autopilot when a world of opportunity is right in front of you. With the right tools, you can spot the next winning trend before the crowd catches on.

- Amplify your returns by targeting high-potential opportunities with these 3577 penny stocks with strong financials, which stand out for strong financials and resilience in volatile markets.

- Unleash the power of tomorrow by riding the wave of disruption in artificial intelligence with these 25 AI penny stocks positioned for industry leadership.

- Secure steady income and portfolio stability by selecting from these 15 dividend stocks with yields > 3%, which offer yields above 3% and can reward patient investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1

CK Hutchison Holdings

An investment holding company, primarily operates in ports and related services, retail, infrastructure, and telecommunications businesses in Hong Kong, Mainland China, Europe, Canada, Asia, Australia, and internationally.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative