Advertisement

Should You Buy Bank of Tianjin Co., Ltd. (HKG:1578) For Its Dividend?

Dividend paying stocks like Bank of Tianjin Co., Ltd. (HKG:1578) tend to be popular with investors, and for good reason - some research suggests a significant amount of all stock market returns come from reinvested dividends. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

With a goodly-sized dividend yield despite a relatively short payment history, investors might be wondering if Bank of Tianjin is a new dividend aristocrat in the making. It sure looks interesting on these metrics - but there's always more to the story. Some simple research can reduce the risk of buying Bank of Tianjin for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on Bank of Tianjin!

Payout ratios

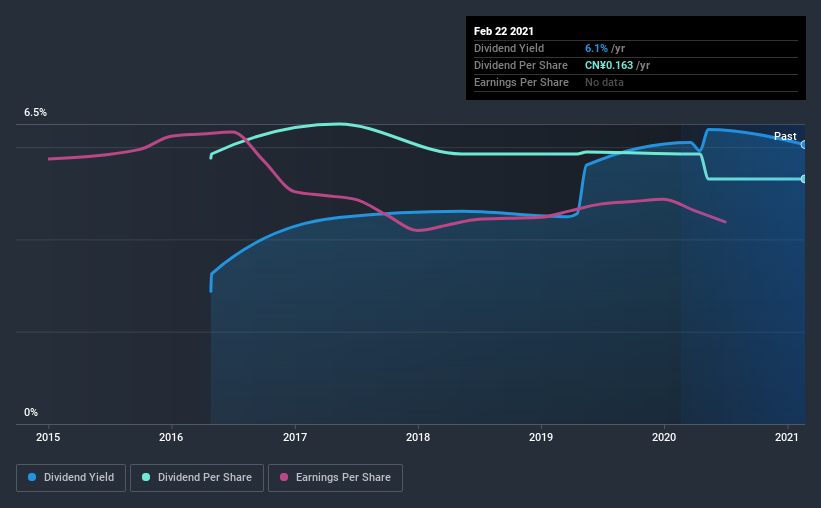

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Bank of Tianjin paid out 27% of its profit as dividends, over the trailing twelve month period. A medium payout ratio strikes a good balance between paying dividends, and keeping enough back to invest in the business. One of the risks is that management reinvests the retained capital poorly instead of paying a higher dividend.

Remember, you can always get a snapshot of Bank of Tianjin's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the data, we can see that Bank of Tianjin has been paying a dividend for the past five years. During the past five-year period, the first annual payment was CN¥0.2 in 2016, compared to CN¥0.2 last year. The dividend has shrunk at around 1.6% a year during that period.

We struggle to make a case for buying Bank of Tianjin for its dividend, given that payments have shrunk over the past five years.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. It's not great to see that Bank of Tianjin's have fallen at approximately 6.0% over the past five years. Declining earnings per share over a number of years is not a great sign for the dividend investor. Without some improvement, this does not bode well for the long term value of a company's dividend.

Conclusion

To summarise, shareholders should always check that Bank of Tianjin's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. We're glad to see Bank of Tianjin has a low payout ratio, as this suggests earnings are being reinvested in the business. Earnings per share have been falling, and the company has a relatively short dividend history - shorter than we like, anyway. Bank of Tianjin might not be a bad business, but it doesn't show all of the characteristics we look for in a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 2 warning signs for Bank of Tianjin (of which 1 makes us a bit uncomfortable!) you should know about.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you decide to trade Bank of Tianjin, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bank of Tianjin might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1578

Bank of Tianjin

Provides a range of banking and related financial services primarily in the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor