Advertisement

- Hong Kong

- /

- Auto Components

- /

- SEHK:1274

The Price Is Right For iMotion Automotive Technology (Suzhou) Co., Ltd. (HKG:1274) Even After Diving 40%

The iMotion Automotive Technology (Suzhou) Co., Ltd. (HKG:1274) share price has softened a substantial 40% over the previous 30 days, handing back much of the gains the stock has made lately. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 85% loss during that time.

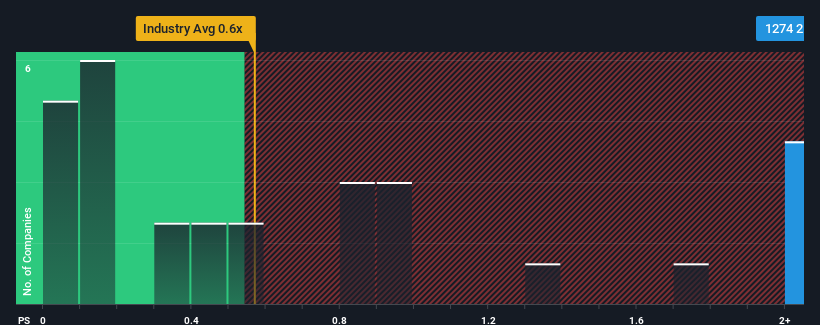

Although its price has dipped substantially, given close to half the companies operating in Hong Kong's Auto Components industry have price-to-sales ratios (or "P/S") below 0.6x, you may still consider iMotion Automotive Technology (Suzhou) as a stock to potentially avoid with its 2.4x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for iMotion Automotive Technology (Suzhou)

How iMotion Automotive Technology (Suzhou) Has Been Performing

iMotion Automotive Technology (Suzhou) could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on iMotion Automotive Technology (Suzhou) will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should outperform the industry for P/S ratios like iMotion Automotive Technology (Suzhou)'s to be considered reasonable.

Retrospectively, the last year delivered a decent 2.6% gain to the company's revenues. The latest three year period has seen an incredible overall rise in revenue, even though the last 12 month performance was only fair. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 52% per annum over the next three years. That's shaping up to be materially higher than the 19% each year growth forecast for the broader industry.

With this in mind, it's not hard to understand why iMotion Automotive Technology (Suzhou)'s P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Despite the recent share price weakness, iMotion Automotive Technology (Suzhou)'s P/S remains higher than most other companies in the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that iMotion Automotive Technology (Suzhou) maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Auto Components industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You need to take note of risks, for example - iMotion Automotive Technology (Suzhou) has 3 warning signs (and 2 which are potentially serious) we think you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if iMotion Automotive Technology (Suzhou) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1274

iMotion Automotive Technology (Suzhou)

Engages in the research and development, production, and sales of autonomous driving (AD) products and solutions in the People’s Republic of China.

Excellent balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|10.4% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|12.4% undervalued

AN

Based on Analyst Price Targets