Advertisement

- Greece

- /

- Specialty Stores

- /

- ATSE:EVR

Optimistic Investors Push I.Kloukinas-I.Lappas S.A. (ATH:KLM) Shares Up 28% But Growth Is Lacking

Despite an already strong run, I.Kloukinas-I.Lappas S.A. (ATH:KLM) shares have been powering on, with a gain of 28% in the last thirty days. The annual gain comes to 218% following the latest surge, making investors sit up and take notice.

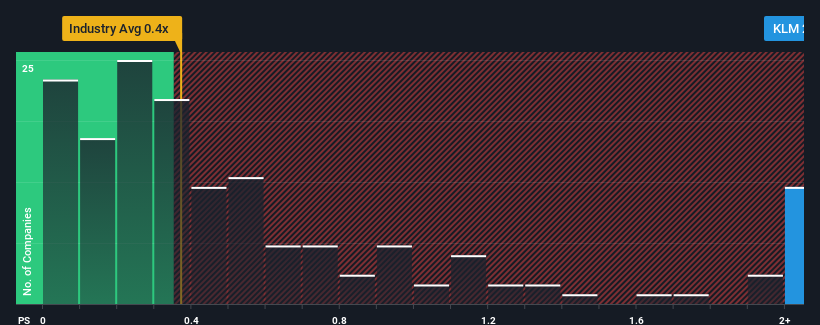

After such a large jump in price, you could be forgiven for thinking I.Kloukinas-I.Lappas is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.2x, considering almost half the companies in Greece's Specialty Retail industry have P/S ratios below 1x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for I.Kloukinas-I.Lappas

How Has I.Kloukinas-I.Lappas Performed Recently?

I.Kloukinas-I.Lappas certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. The P/S ratio is probably high because investors think this strong revenue growth will be enough to outperform the broader industry in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on I.Kloukinas-I.Lappas' earnings, revenue and cash flow.How Is I.Kloukinas-I.Lappas' Revenue Growth Trending?

In order to justify its P/S ratio, I.Kloukinas-I.Lappas would need to produce impressive growth in excess of the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 76%. As a result, it also grew revenue by 7.6% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

This is in contrast to the rest of the industry, which is expected to grow by 7.4% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we find it concerning that I.Kloukinas-I.Lappas is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

The large bounce in I.Kloukinas-I.Lappas' shares has lifted the company's P/S handsomely. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of I.Kloukinas-I.Lappas revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. Right now we aren't comfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

You should always think about risks. Case in point, we've spotted 3 warning signs for I.Kloukinas-I.Lappas you should be aware of, and 1 of them is a bit unpleasant.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Evropi Holdings Societe Anonyme might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:EVR

Evropi Holdings Societe Anonyme

Engages in construction businesses in Greece.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor