Advertisement

- Greece

- /

- Oil and Gas

- /

- ATSE:ELPE

Hellenic Petroleum Holdings Societe Anonyme (ATH:ELPE) Takes On Some Risk With Its Use Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Hellenic Petroleum Holdings Societe Anonyme (ATH:ELPE) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Hellenic Petroleum Holdings Societe Anonyme

What Is Hellenic Petroleum Holdings Societe Anonyme's Debt?

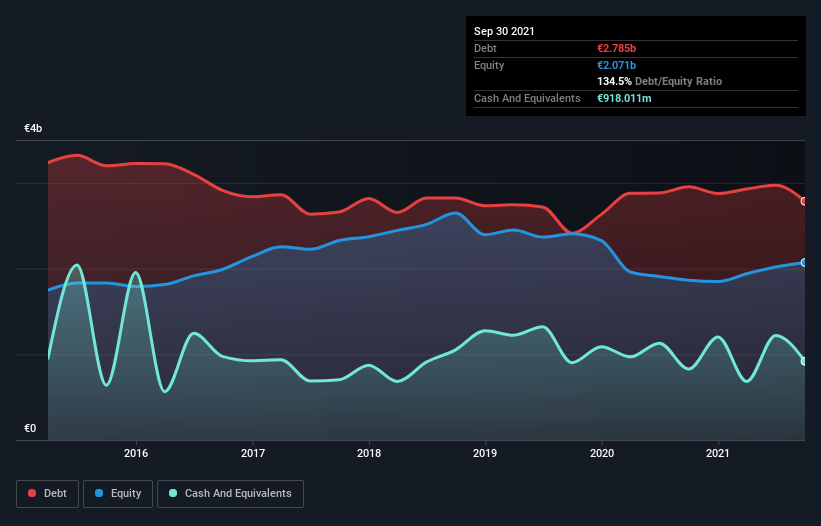

The image below, which you can click on for greater detail, shows that Hellenic Petroleum Holdings Societe Anonyme had debt of €2.78b at the end of September 2021, a reduction from €2.95b over a year. On the flip side, it has €918.0m in cash leading to net debt of about €1.87b.

How Healthy Is Hellenic Petroleum Holdings Societe Anonyme's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hellenic Petroleum Holdings Societe Anonyme had liabilities of €2.50b due within 12 months and liabilities of €2.52b due beyond that. Offsetting this, it had €918.0m in cash and €577.0m in receivables that were due within 12 months. So it has liabilities totalling €3.53b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the €2.00b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Hellenic Petroleum Holdings Societe Anonyme would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hellenic Petroleum Holdings Societe Anonyme's debt is 3.2 times its EBITDA, and its EBIT cover its interest expense 4.2 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. One redeeming factor for Hellenic Petroleum Holdings Societe Anonyme is that it turned last year's EBIT loss into a gain of €377m, over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hellenic Petroleum Holdings Societe Anonyme can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, Hellenic Petroleum Holdings Societe Anonyme actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Mulling over Hellenic Petroleum Holdings Societe Anonyme's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Once we consider all the factors above, together, it seems to us that Hellenic Petroleum Holdings Societe Anonyme's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Hellenic Petroleum Holdings Societe Anonyme (including 1 which can't be ignored) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if HELLENiQ ENERGY Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:ELPE

HELLENiQ ENERGY Holdings

Operates in the energy sector in Greece, the Southeastern Europe, and the East Mediterranean.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor