Advertisement

- Greece

- /

- Hospitality

- /

- ATSE:KYRI

The Market Doesn't Like What It Sees From Kiriacoulis Mediterranean Cruises Shipping SA's (ATH:KYRI) Revenues Yet

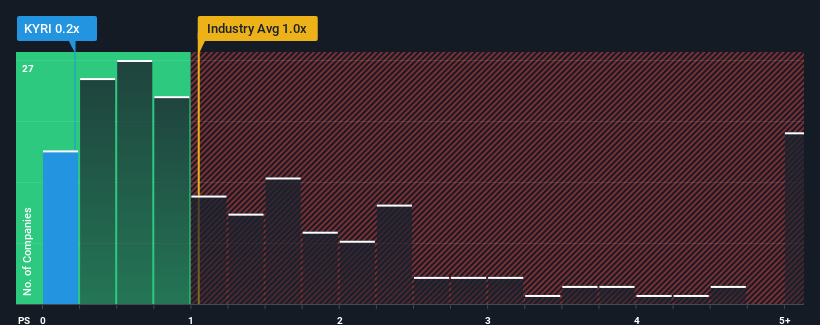

When close to half the companies in the Hospitality industry in Greece have price-to-sales ratios (or "P/S") above 5.7x, you may consider Kiriacoulis Mediterranean Cruises Shipping SA (ATH:KYRI) as a highly attractive investment with its 0.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Check out our latest analysis for Kiriacoulis Mediterranean Cruises Shipping

What Does Kiriacoulis Mediterranean Cruises Shipping's P/S Mean For Shareholders?

Recent times have been quite advantageous for Kiriacoulis Mediterranean Cruises Shipping as its revenue has been rising very briskly. Perhaps the market is expecting future revenue performance to dwindle, which has kept the P/S suppressed. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Although there are no analyst estimates available for Kiriacoulis Mediterranean Cruises Shipping, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Kiriacoulis Mediterranean Cruises Shipping's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as depressed as Kiriacoulis Mediterranean Cruises Shipping's is when the company's growth is on track to lag the industry decidedly.

If we review the last year of revenue growth, the company posted a terrific increase of 43%. The strong recent performance means it was also able to grow revenue by 46% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 72% shows it's noticeably less attractive.

With this in consideration, it's easy to understand why Kiriacoulis Mediterranean Cruises Shipping's P/S falls short of the mark set by its industry peers. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

The Bottom Line On Kiriacoulis Mediterranean Cruises Shipping's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Kiriacoulis Mediterranean Cruises Shipping revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for Kiriacoulis Mediterranean Cruises Shipping (3 are significant) you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kiriacoulis Mediterranean Cruises Shipping might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:KYRI

Kiriacoulis Mediterranean Cruises Shipping

Engages in the professional sea tourism, tourist ports management, and real estate businesses.

Low risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets