- United Kingdom

- /

- Commercial Services

- /

- AIM:HSP

Exploring Undiscovered Gems in the UK Stock Market March 2025

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 index slipping due to weak trade data from China, highlighting global economic interdependencies and their impact on local markets. Despite these broader market setbacks, opportunities remain in the small-cap sector where investors often seek companies with strong fundamentals and growth potential that might be overlooked amid larger economic concerns.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Livermore Investments Group | NA | 9.92% | 13.65% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -7.93% | -8.41% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| FW Thorpe | 2.95% | 11.79% | 13.49% | ★★★★★☆ |

| Goodwin | 37.02% | 9.75% | 15.68% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| AltynGold | 77.07% | 28.64% | 38.10% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Griffin Mining (AIM:GFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Griffin Mining Limited is a mining and investment company focused on the exploration and development of mineral properties, with a market capitalization of £346.46 million.

Operations: Griffin Mining generates revenue primarily from the Caijiaying Zinc Gold Mine, with reported earnings of $162.25 million.

Griffin Mining, a nimble player in the UK mining sector, has been making waves with its impressive earnings growth of 116% over the past year, outpacing the broader Metals and Mining industry. The company operates debt-free and boasts high-quality earnings, positioning it as a solid contender in its field. Despite a dip in zinc production to 39,444 tonnes from last year's 56,933 tonnes due to operational halts at Caijiaying Mine now resumed operations are likely to stabilize output. Trading at 16% below estimated fair value suggests potential upside for investors eyeing this under-the-radar stock.

- Click here and access our complete health analysis report to understand the dynamics of Griffin Mining.

Evaluate Griffin Mining's historical performance by accessing our past performance report.

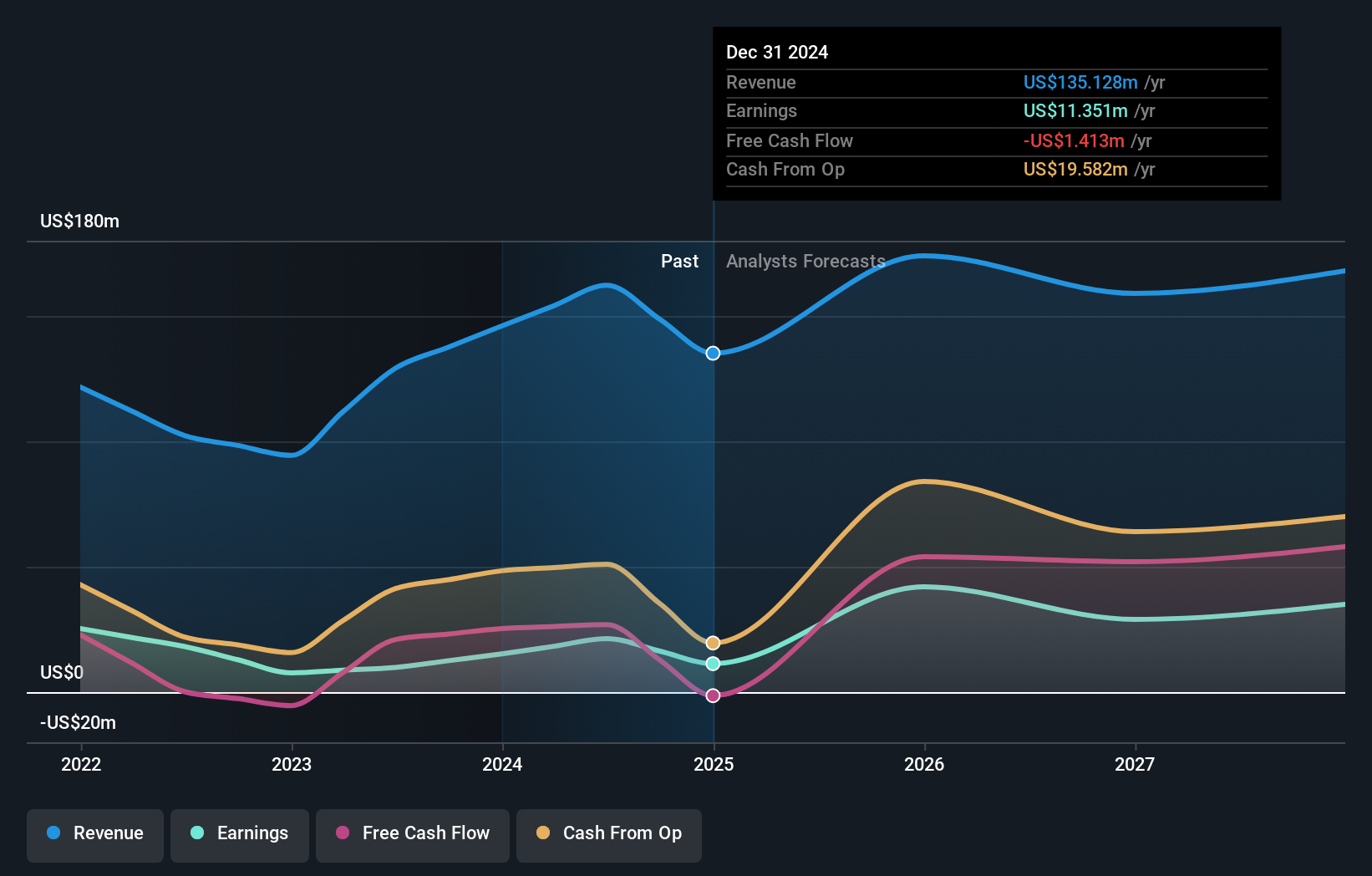

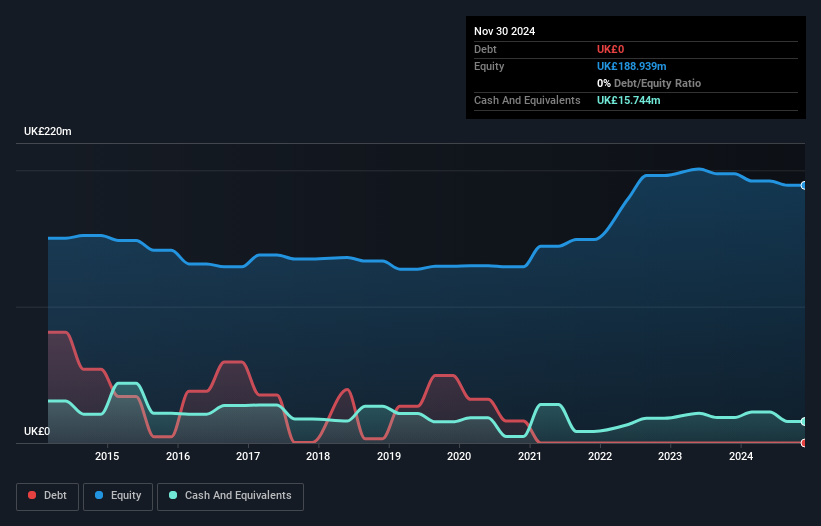

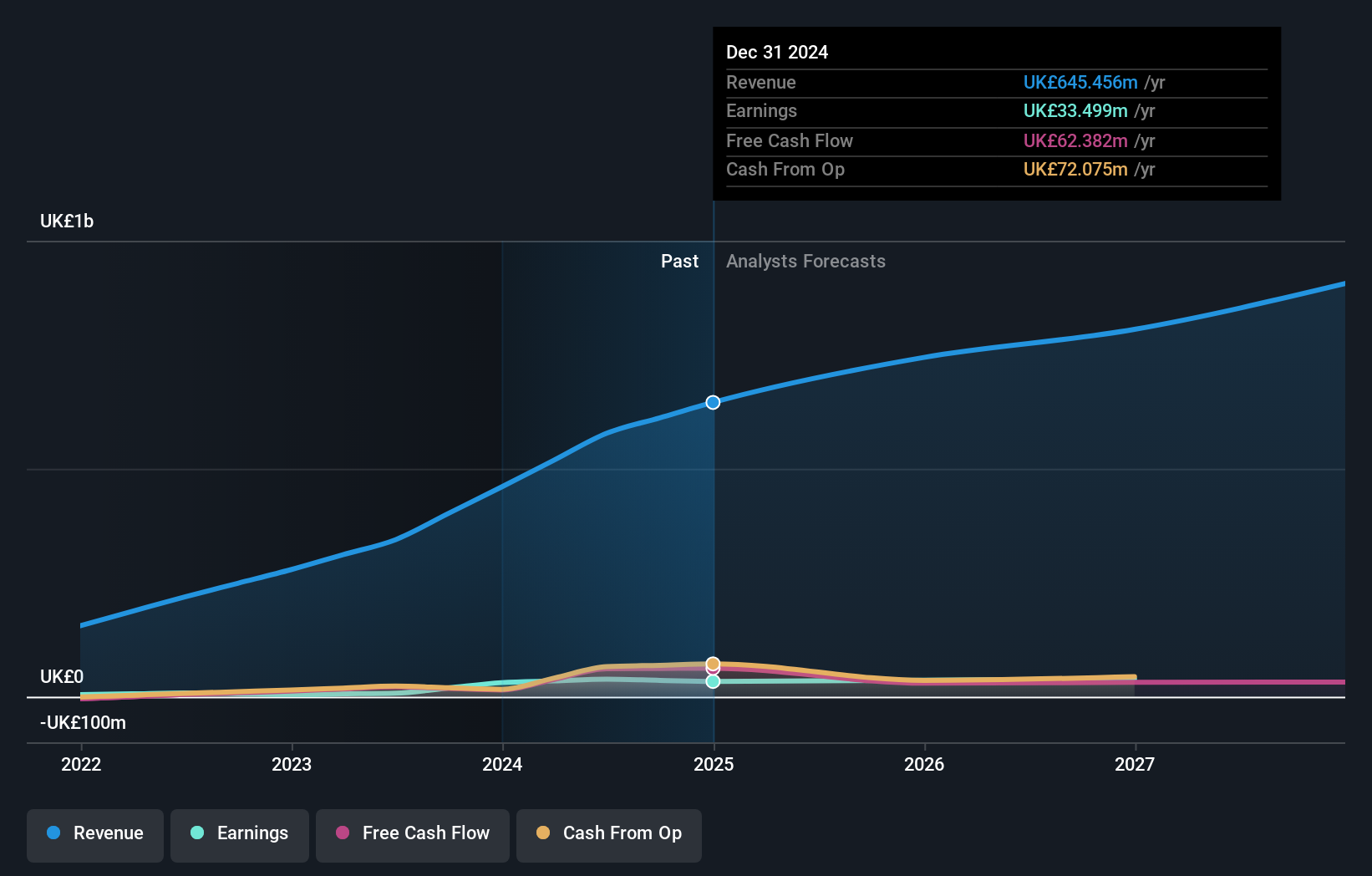

Hargreaves Services (AIM:HSP)

Simply Wall St Value Rating: ★★★★★★

Overview: Hargreaves Services Plc offers environmental and industrial services across the United Kingdom, Europe, Hong Kong, and other international markets with a market capitalization of £214.91 million.

Operations: The company generates revenue primarily from its services segment, amounting to £219.11 million, with a smaller contribution from Hargreaves Land at £10.54 million.

Hargreaves Services, a UK-based company with a focus on infrastructure and energy markets, has shown promising performance. Over the past year, earnings grew by 15%, outpacing the Oil and Gas industry which saw a -46.9% shift. The firm reported sales of £125.34 million for the half-year ending November 2024, up from £110.17 million in 2023, while net income rose to £3.99 million from £1.71 million previously. Notably debt-free now compared to five years ago when its debt-to-equity ratio was 38%, HSP also declared an increased interim dividend of 18.5 pence per share for April 2025 payments.

- Navigate through the intricacies of Hargreaves Services with our comprehensive health report here.

Examine Hargreaves Services' past performance report to understand how it has performed in the past.

Yü Group (AIM:YU.)

Simply Wall St Value Rating: ★★★★★☆

Overview: Yü Group PLC, with a market cap of £247.65 million, supplies energy and utility solutions primarily in the United Kingdom through its subsidiaries.

Operations: Yü Group generates revenue by supplying energy and utility solutions in the UK. The company's net profit margin has shown an interesting trend, reflecting its financial performance over time.

Yü Group, a small player in the UK energy sector, has shown impressive earnings growth of 400% over the past year, outpacing the industry average. Despite an increase in its debt to equity ratio from 0% to 5% over five years, it maintains more cash than total debt, indicating solid financial health. The company trades at a notable discount of 32.7% below its estimated fair value and is expected to continue revenue growth at about 16% annually. However, earnings are projected to decrease by an average of 1.7% per year for the next three years.

- Get an in-depth perspective on Yü Group's performance by reading our health report here.

Assess Yü Group's past performance with our detailed historical performance reports.

Make It Happen

- Gain an insight into the universe of 63 UK Undiscovered Gems With Strong Fundamentals by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hargreaves Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:HSP

Hargreaves Services

Provides environmental and industrial services in the United Kingdom, Europe, Hong Kong, and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion