- United Kingdom

- /

- Airlines

- /

- LSE:WIZZ

Analyst Estimates: Here's What Brokers Think Of Wizz Air Holdings Plc (LON:WIZZ) After Its First-Quarter Report

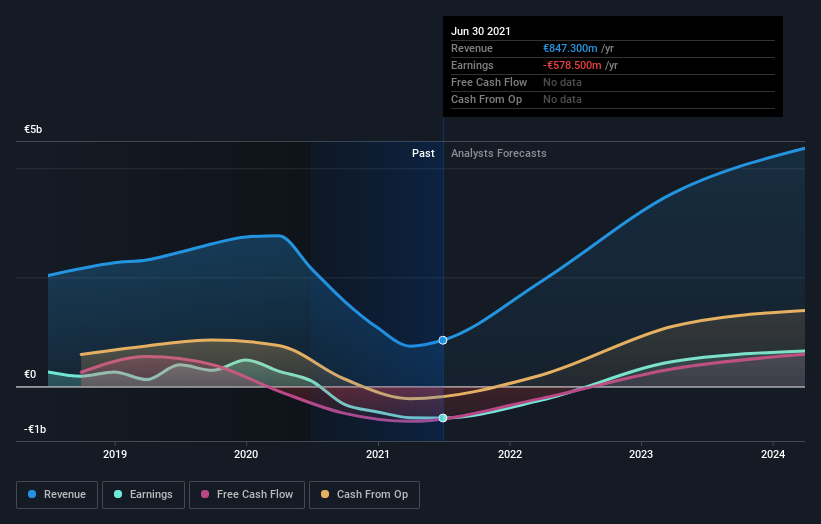

It's been a good week for Wizz Air Holdings Plc (LON:WIZZ) shareholders, because the company has just released its latest first-quarter results, and the shares gained 8.8% to UK£49.50. Revenues were €199m, with Wizz Air Holdings reporting some 8.6% below analyst expectations. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Wizz Air Holdings

Following the latest results, Wizz Air Holdings' 23 analysts are now forecasting revenues of €1.93b in 2022. This would be a substantial 128% improvement in sales compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 69% to €2.05. Yet prior to the latest earnings, the analysts had been forecasting revenues of €1.90b and losses of €1.07 per share in 2022. So it's pretty clear the analysts have mixed opinions on Wizz Air Holdings even after this update; although they reconfirmed their revenue numbers, it came at the cost of a regrettable increase in per-share losses.

The consensus price target held steady at UK£51.95, seemingly implying that the higher forecast losses are not expected to have a long term impact on the company's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Wizz Air Holdings, with the most bullish analyst valuing it at UK£67.53 and the most bearish at UK£37.59 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Wizz Air Holdings shareholders.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Wizz Air Holdings' past performance and to peers in the same industry. One thing stands out from these estimates, which is that Wizz Air Holdings is forecast to grow faster in the future than it has in the past, with revenues expected to display 200% annualised growth until the end of 2022. If achieved, this would be a much better result than the 0.8% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 33% annually. Not only are Wizz Air Holdings' revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Wizz Air Holdings. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Wizz Air Holdings analysts - going out to 2024, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Wizz Air Holdings (1 makes us a bit uncomfortable!) that you need to be mindful of.

If you decide to trade Wizz Air Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wizz Air Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:WIZZ

Wizz Air Holdings

Engages in the provision of passenger air transportation services.

High growth potential with proven track record.

Similar Companies

Market Insights

Community Narratives