Advertisement

- United Kingdom

- /

- Capital Markets

- /

- AIM:LDG

Here's What Eddie Stobart Logistics plc's (LON:ESL) P/E Is Telling Us

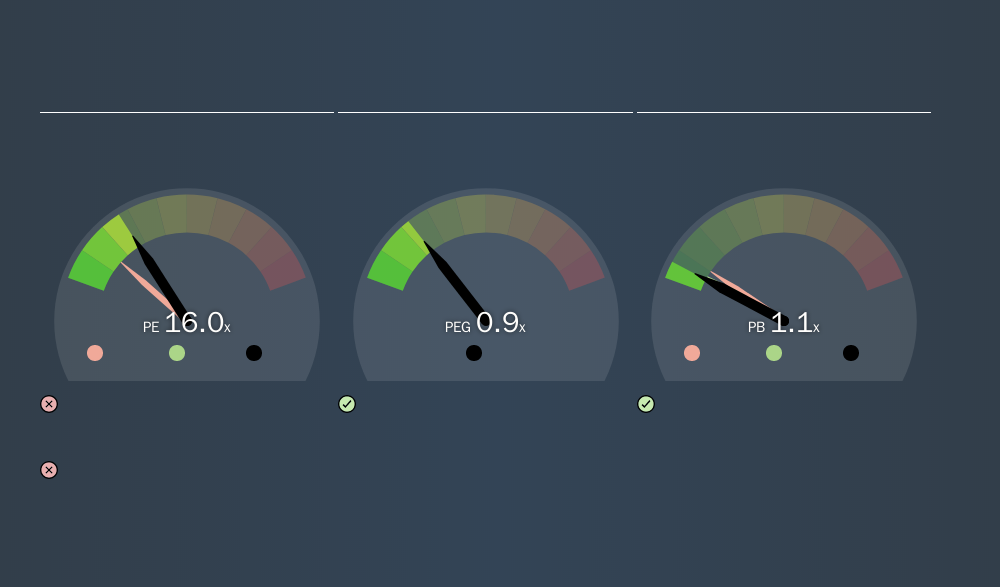

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll apply a basic P/E ratio analysis to Eddie Stobart Logistics plc's (LON:ESL), to help you decide if the stock is worth further research. Eddie Stobart Logistics has a P/E ratio of 16.04, based on the last twelve months. That corresponds to an earnings yield of approximately 6.2%.

See our latest analysis for Eddie Stobart Logistics

How Do I Calculate A Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Eddie Stobart Logistics:

P/E of 16.04 = £0.71 ÷ £0.044 (Based on the year to November 2018.)

Is A High Price-to-Earnings Ratio Good?

The higher the P/E ratio, the higher the price tag of a business, relative to its trailing earnings. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.'

How Does Eddie Stobart Logistics's P/E Ratio Compare To Its Peers?

The P/E ratio indicates whether the market has higher or lower expectations of a company. As you can see below, Eddie Stobart Logistics has a higher P/E than the average company (9.7) in the transportation industry.

That means that the market expects Eddie Stobart Logistics will outperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. Earnings growth means that in the future the 'E' will be higher. And in that case, the P/E ratio itself will drop rather quickly. Then, a lower P/E should attract more buyers, pushing the share price up.

In the last year, Eddie Stobart Logistics grew EPS like Taylor Swift grew her fan base back in 2010; the 265% gain was both fast and well deserved. Even better, EPS is up 40% per year over three years. So you might say it really deserves to have an above-average P/E ratio.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. That means it doesn't take debt or cash into account. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Eddie Stobart Logistics's Balance Sheet

Net debt totals 56% of Eddie Stobart Logistics's market cap. This is enough debt that you'd have to make some adjustments before using the P/E ratio to compare it to a company with net cash.

The Verdict On Eddie Stobart Logistics's P/E Ratio

Eddie Stobart Logistics trades on a P/E ratio of 16, which is fairly close to the GB market average of 16. The significant levels of debt do detract somewhat from the strong earnings growth. The P/E suggests that the market is not convinced EPS will continue to improve strongly.

Investors should be looking to buy stocks that the market is wrong about. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About AIM:LDG

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor