Advertisement

- United Kingdom

- /

- Wireless Telecom

- /

- LSE:AAF

We Like These Underlying Return On Capital Trends At Airtel Africa (LON:AAF)

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Airtel Africa (LON:AAF) so let's look a bit deeper.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Airtel Africa, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

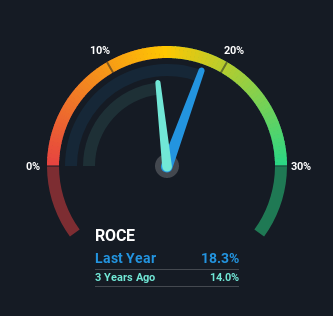

0.18 = US$1.3b ÷ (US$9.7b - US$2.8b) (Based on the trailing twelve months to June 2021).

Therefore, Airtel Africa has an ROCE of 18%. On its own, that's a standard return, however it's much better than the 9.0% generated by the Wireless Telecom industry.

See our latest analysis for Airtel Africa

In the above chart we have measured Airtel Africa's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

The Trend Of ROCE

We like the trends that we're seeing from Airtel Africa. The data shows that returns on capital have increased substantially over the last four years to 18%. The amount of capital employed has increased too, by 42%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

On a related note, the company's ratio of current liabilities to total assets has decreased to 29%, which basically reduces it's funding from the likes of short-term creditors or suppliers. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

In Conclusion...

All in all, it's terrific to see that Airtel Africa is reaping the rewards from prior investments and is growing its capital base. And with a respectable 62% awarded to those who held the stock over the last year, you could argue that these developments are starting to get the attention they deserve. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

On a final note, we've found 2 warning signs for Airtel Africa that we think you should be aware of.

While Airtel Africa may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Airtel Africa or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:AAF

Airtel Africa

Provides telecommunications and mobile money services in Nigeria, East Africa, and Francophone Africa.

High growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor