- United Kingdom

- /

- Communications

- /

- LSE:SPT

The Spirent Communications plc (LON:SPT) Full-Year Results Are Out And Analysts Have Published New Forecasts

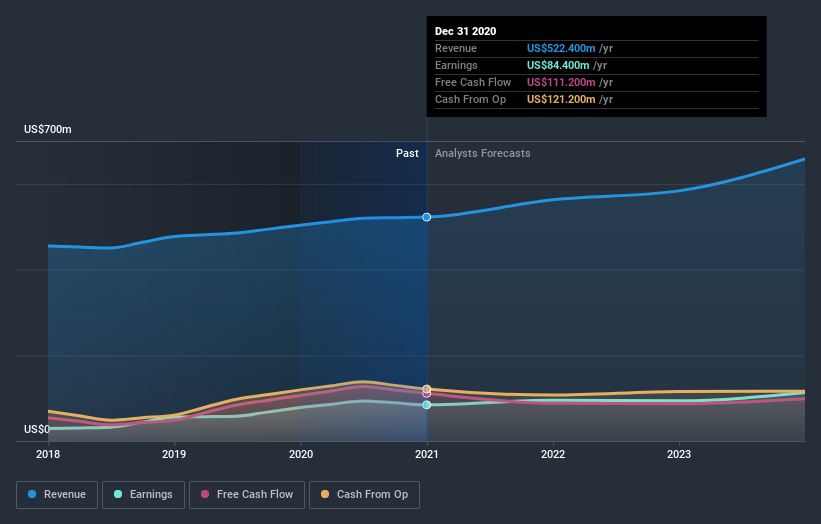

The yearly results for Spirent Communications plc (LON:SPT) were released last week, making it a good time to revisit its performance. Results were roughly in line with estimates, with revenues of US$522m and statutory earnings per share of US$0.13. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Spirent Communications after the latest results.

See our latest analysis for Spirent Communications

Taking into account the latest results, the most recent consensus for Spirent Communications from seven analysts is for revenues of US$562.8m in 2021 which, if met, would be a reasonable 7.7% increase on its sales over the past 12 months. Per-share earnings are expected to rise 4.5% to US$0.14. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$561.4m and earnings per share (EPS) of US$0.15 in 2021. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

It might be a surprise to learn that the consensus price target was broadly unchanged at UK£2.72, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Spirent Communications at UK£3.30 per share, while the most bearish prices it at UK£1.75. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Spirent Communications' rate of growth is expected to accelerate meaningfully, with the forecast 7.7% annualised revenue growth to the end of 2021 noticeably faster than its historical growth of 2.5% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 5.8% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Spirent Communications is expected to grow much faster than its industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Spirent Communications. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Spirent Communications going out to 2023, and you can see them free on our platform here..

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Spirent Communications , and understanding this should be part of your investment process.

If you’re looking to trade Spirent Communications, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:SPT

Spirent Communications

As of October 15, 2025, operates as a subsidiary of Keysight Technologies, Inc..

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion