Advertisement

Results: Oxford Instruments plc Beat Earnings Expectations And Analysts Now Have New Forecasts

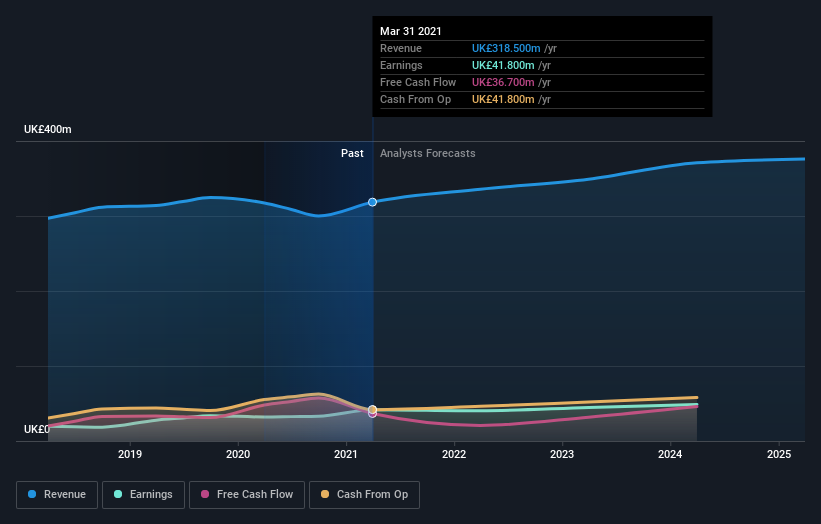

The yearly results for Oxford Instruments plc (LON:OXIG) were released last week, making it a good time to revisit its performance. The result was positive overall - although revenues of UK£319m were in line with what the analysts predicted, Oxford Instruments surprised by delivering a statutory profit of UK£0.72 per share, modestly greater than expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Oxford Instruments after the latest results.

Check out our latest analysis for Oxford Instruments

Following the latest results, Oxford Instruments' seven analysts are now forecasting revenues of UK£335.7m in 2022. This would be a modest 5.4% improvement in sales compared to the last 12 months. Statutory earnings per share are forecast to decrease 7.4% to UK£0.67 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of UK£336.3m and earnings per share (EPS) of UK£0.76 in 2022. So there's definitely been a decline in sentiment after the latest results, noting the substantial drop in new EPS forecasts.

The consensus price target held steady at UK£24.02, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Oxford Instruments at UK£26.35 per share, while the most bearish prices it at UK£21.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Oxford Instruments' rate of growth is expected to accelerate meaningfully, with the forecast 5.4% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 1.1% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 7.3% per year. It seems obvious that, while the future growth outlook is brighter than the recent past, Oxford Instruments is expected to grow slower than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Oxford Instruments' revenues are expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Oxford Instruments going out to 2025, and you can see them free on our platform here.

We also provide an overview of the Oxford Instruments Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

If you’re looking to trade Oxford Instruments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:OXIG

Oxford Instruments

Oxford Instruments plc provide scientific technology products and services for academic and commercial organizations worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor