Advertisement

We Think Seeing Machines (LON:SEE) Can Afford To Drive Business Growth

Just because a business does not make any money, does not mean that the stock will go down. For example, Seeing Machines (LON:SEE) shareholders have done very well over the last year, with the share price soaring by 294%. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So notwithstanding the buoyant share price, we think it's well worth asking whether Seeing Machines' cash burn is too risky. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Seeing Machines

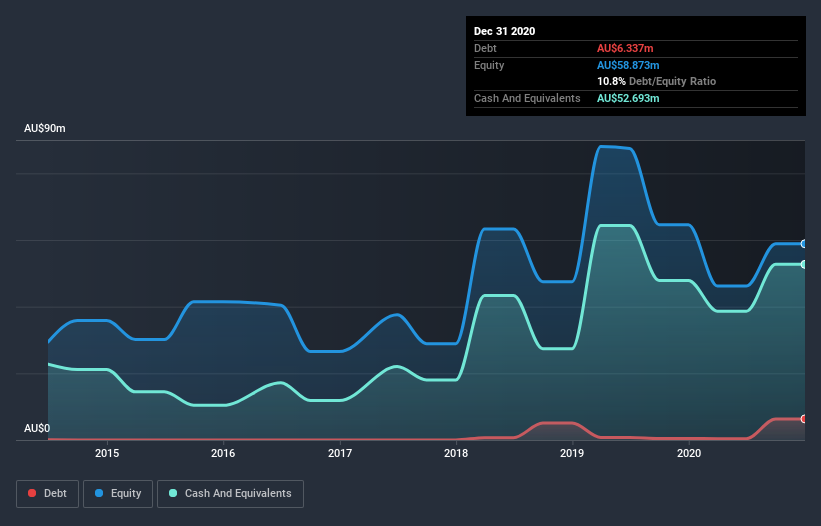

How Long Is Seeing Machines' Cash Runway?

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. Seeing Machines has such a small amount of debt that we'll set it aside, and focus on the AU$53m in cash it held at December 2020. Importantly, its cash burn was AU$22m over the trailing twelve months. So it had a cash runway of about 2.4 years from December 2020. Importantly, analysts think that Seeing Machines will reach cashflow breakeven in 3 years. So there's a very good chance it won't need more cash, when you consider the burn rate will be reducing in that period. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Seeing Machines Growing?

We reckon the fact that Seeing Machines managed to shrink its cash burn by 30% over the last year is rather encouraging. And considering that its operating revenue gained 26% during that period, that's great to see. It seems to be growing nicely. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For Seeing Machines To Raise More Cash For Growth?

We are certainly impressed with the progress Seeing Machines has made over the last year, but it is also worth considering how costly it would be if it wanted to raise more cash to fund faster growth. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Seeing Machines has a market capitalisation of AU$678m and burnt through AU$22m last year, which is 3.2% of the company's market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

Is Seeing Machines' Cash Burn A Worry?

As you can probably tell by now, we're not too worried about Seeing Machines' cash burn. For example, we think its cash burn relative to its market cap suggests that the company is on a good path. Its cash burn reduction wasn't quite as good, but was still rather encouraging! Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. An in-depth examination of risks revealed 3 warning signs for Seeing Machines that readers should think about before committing capital to this stock.

Of course Seeing Machines may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Seeing Machines or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:SEE

Seeing Machines

Provides driver and occupant monitoring system technologies in Australia, North America, the Asia Pacific, Europe, and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor