Advertisement

- United Kingdom

- /

- IT

- /

- LSE:FDM

Are FDM Group (Holdings) plc's (LON:FDM) Mixed Financials The Reason For Its Gloomy Performance on The Stock Market?

With its stock down 17% over the past three months, it is easy to disregard FDM Group (Holdings) (LON:FDM). It seems that the market might have completely ignored the positive aspects of the company's fundamentals and decided to weigh-in more on the negative aspects. Fundamentals usually dictate market outcomes so it makes sense to study the company's financials. Specifically, we decided to study FDM Group (Holdings)'s ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for FDM Group (Holdings)

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for FDM Group (Holdings) is:

50% = UK£39m ÷ UK£79m (Based on the trailing twelve months to June 2023).

The 'return' is the income the business earned over the last year. So, this means that for every £1 of its shareholder's investments, the company generates a profit of £0.50.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

FDM Group (Holdings)'s Earnings Growth And 50% ROE

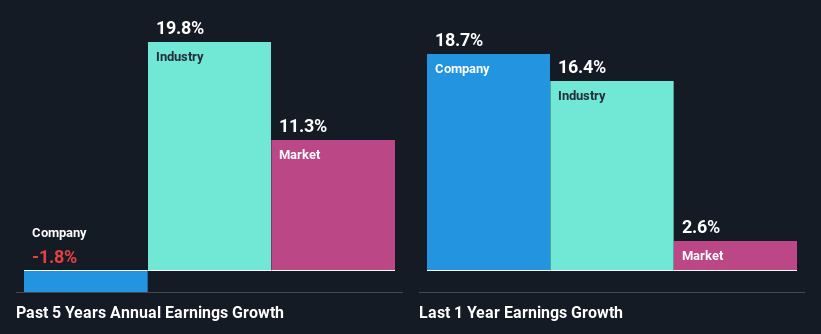

To begin with, FDM Group (Holdings) has a pretty high ROE which is interesting. Secondly, even when compared to the industry average of 9.4% the company's ROE is quite impressive. Given the circumstances, we can't help but wonder why FDM Group (Holdings) saw little to no growth in the past five years. We reckon that there could be some other factors at play here that's limiting the company's growth. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for instance.

Next, on comparing with the industry net income growth, we found that the industry grew its earnings by 20% over the last few years.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for FDM? You can find out in our latest intrinsic value infographic research report.

Is FDM Group (Holdings) Using Its Retained Earnings Effectively?

FDM Group (Holdings)'s very high three-year median payout ratio of 114% suggests that the company is paying its shareholders more than what it is earning. The absence in growth is therefore not surprising. Its usually very hard to sustain dividend payments that are higher than reported profits. That's a huge risk in our books. To know the 2 risks we have identified for FDM Group (Holdings) visit our risks dashboard for free.

Moreover, FDM Group (Holdings) has been paying dividends for eight years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 100%. As a result, FDM Group (Holdings)'s ROE is not expected to change by much either, which we inferred from the analyst estimate of 48% for future ROE.

Conclusion

On the whole, we feel that the performance shown by FDM Group (Holdings) can be open to many interpretations. In spite of the high ROE, the company has failed to see growth in its earnings due to it paying out most of its profits as dividend, with almost nothing left to invest into its own business. Further, on studying current analyst estimates, we found that the company's earnings growth is expected to be pretty much the same. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:FDM

FDM Group (Holdings)

Provides information technology (IT) services in the United Kingdom, North America, Europe, the Middle East, Africa, rest of Europe, and the Asia Pacific.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor