Advertisement

- United Kingdom

- /

- IT

- /

- LSE:CCC

These 4 Measures Indicate That Computacenter (LON:CCC) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Computacenter plc (LON:CCC) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Computacenter

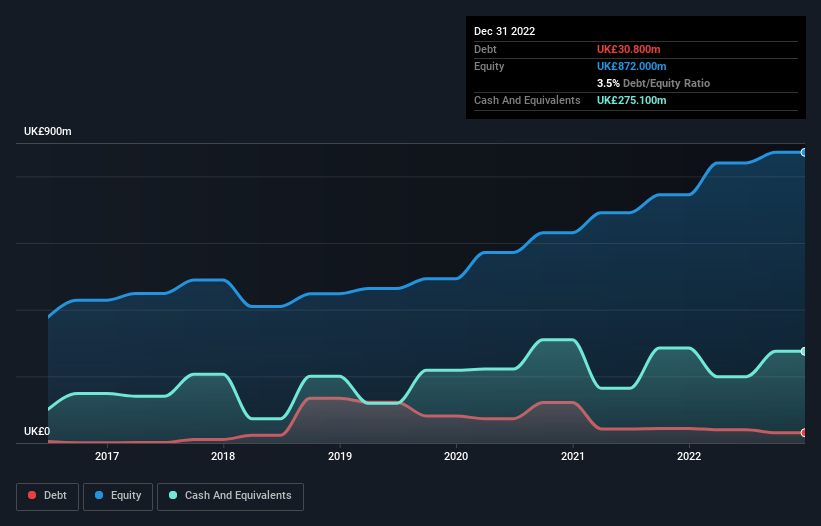

What Is Computacenter's Net Debt?

The image below, which you can click on for greater detail, shows that Computacenter had debt of UK£30.8m at the end of December 2022, a reduction from UK£43.8m over a year. But it also has UK£275.1m in cash to offset that, meaning it has UK£244.3m net cash.

How Strong Is Computacenter's Balance Sheet?

According to the last reported balance sheet, Computacenter had liabilities of UK£2.25b due within 12 months, and liabilities of UK£161.4m due beyond 12 months. Offsetting this, it had UK£275.1m in cash and UK£1.86b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£270.1m.

Given Computacenter has a market capitalization of UK£2.60b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Computacenter also has more cash than debt, so we're pretty confident it can manage its debt safely.

While Computacenter doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Computacenter's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Computacenter may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Computacenter generated free cash flow amounting to a very robust 86% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Summing Up

Although Computacenter's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of UK£244.3m. And it impressed us with free cash flow of UK£207m, being 86% of its EBIT. So is Computacenter's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Computacenter you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CCC

Computacenter

Provides technology and services to corporate and public sector organizations in the United Kingdom, Germany, Western Europe, North America, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.4% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k6.4% undervalued

30 followersusers have followed this narrative

4 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k6.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.123.0% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AL

alex30free on Beijer Ref ·

The Green Consolidator

Fair Value:SEK 128.820.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

BenjaminMartins on EDP ·

EDP as a safe capital allocation with a potential upside of 28% with steady dividends

Fair Value:€514.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Discovery Silver ·

#1 Silver Play with Positive Cashflow Gold Miner (Top Notch Team)

Fair Value:CA$20695.5% undervalued

44 followersusers have followed this narrative

15 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8236.2% undervalued

84 followersusers have followed this narrative

6 commentsusers have commented on this narrative

35 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.6% undervalued

75 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.6% undervalued

1048 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

Trending Discussion

HE

Hemingway on Aeva Technologies ·

NVDA+AEVA Agreement is a game changer for the AEVA stock even though it is just a partnership and does not have a roll out until 2028 (which means receivables as early as 2027, I would imagine) This agreement effectively moves the goal posts of profitability for AEVA much closer since this is in addition to the recent Forterra agreement, as well as the (previously announced) European carmaker agreement (which is believed to be Mercedes-Benz and estimated to be worth at least 1 billion in sales alone) Underneath all of this, AEVA has a pre-existing agreement with Daimler Truck. So business seems to be booming, especially with really big name brands…which tends to bring in even more brand names (and thus more agreements/contracts/announcements, etc). This dynamic often creates more coverage from analysts (often with upside stock initial coverage) that I believe will be occurring over the next 3 to 6 months (as professional traders/analysts often research for 2 to 3 months before initiating coverage of a new issue). I also feel that the above momentum increases the likelihood that companies that do not currently utilize 4G LIDAR technology might consider buying AEVA outright. Realistically, even with a substantial premium to the current stock price, the cost of AEVA would be a rounding error for the likes of a company such as Tesla, and certainly would allow them to maintain their technological edge as the competition for self-driving vehicles continues to heat up. However, I think it is equally possible for NVidea to decide to lock-in the AEVA technology for their upcoming autonomous hardware/software package by buying them outright. Obviously, the above factors and recent activity in the AEVA stock are cause for optimism. Of course, this all just one opinion , so please do your own due diligence. Disclaimer: I/We DO trade in this stock from time to time and I/we may (or may not have) a position currently, so again, please do your own due diligence.

0

|0