Advertisement

- United Kingdom

- /

- IT

- /

- LSE:CCC

Computacenter (LON:CCC) Has Announced That It Will Be Increasing Its Dividend To UK£0.49

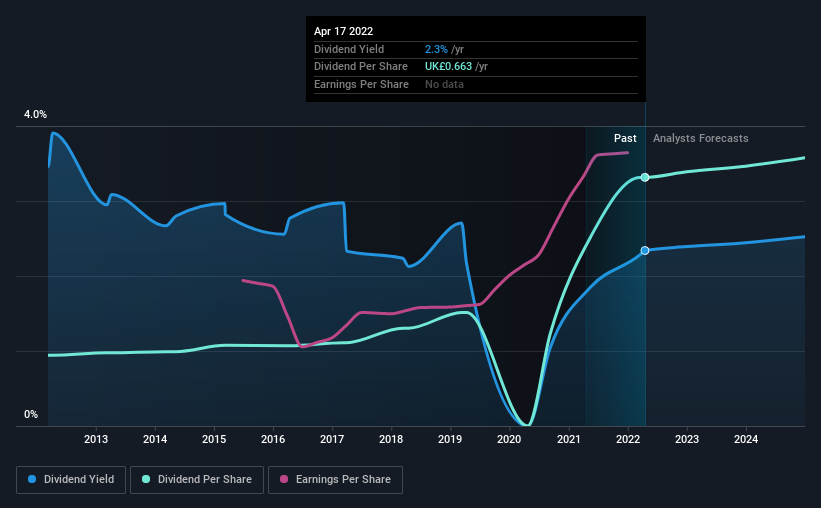

Computacenter plc's (LON:CCC) dividend will be increasing to UK£0.49 on 8th of July. The announced payment will take the dividend yield to 2.3%, which is in line with the average for the industry.

Check out our latest analysis for Computacenter

Computacenter's Earnings Easily Cover the Distributions

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Prior to this announcement, Computacenter's dividend was comfortably covered by both cash flow and earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

EPS is set to fall by 2.7% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio could be 48%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. Since 2012, the first annual payment was UK£0.19, compared to the most recent full-year payment of UK£0.66. This means that it has been growing its distributions at 13% per annum over that time. Computacenter has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Computacenter has seen EPS rising for the last five years, at 25% per annum. The company doesn't have any problems growing, despite returning a lot of capital to shareholders, which is a very nice combination for a dividend stock to have.

Computacenter Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for Computacenter that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CCC

Computacenter

Provides technology and services to corporate and public sector organizations in the United Kingdom, Germany, Western Europe, North America, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.8% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AG

AgWiz on Ingredion ·

Ingredion's Future PE of 9.5x Will Make Waves in the Investment Community

Fair Value:US$88.2311.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LY

Lyra on DT Cloud Star Acquisition ·

A SPAC in the Endgame Between Lifeboat and Siren Song

Fair Value:US$6.1584.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative