Advertisement

- United Kingdom

- /

- Hospitality

- /

- LSE:BOWL

Top 3 European Undervalued Small Caps With Insider Buying In March 2025

Simply Wall St

Reviewed by Simply Wall St

The European market has recently shown signs of resilience, with the pan-European STOXX Europe 600 Index ending higher after two weeks of losses, buoyed by hopes of increased government spending despite ongoing concerns about U.S. tariffs. In this context, small-cap stocks in Europe can present unique opportunities for investors seeking growth potential and diversification, particularly when insider buying signals confidence in a company's future prospects amidst a complex economic landscape.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| J D Wetherspoon | 10.8x | 0.3x | 40.12% | ★★★★★★ |

| Bytes Technology Group | 22.9x | 5.8x | 10.12% | ★★★★★☆ |

| Macfarlane Group | 10.7x | 0.6x | 39.18% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 48.30% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 23.90% | ★★★★★☆ |

| Foxtons Group | 13.7x | 1.2x | 26.43% | ★★★★★☆ |

| Savills | 25.1x | 0.6x | 36.03% | ★★★★☆☆ |

| FRP Advisory Group | 12.5x | 2.2x | 8.59% | ★★★☆☆☆ |

| Arendals Fossekompani | 20.6x | 1.6x | 47.83% | ★★★☆☆☆ |

| Franchise Brands | 36.2x | 1.9x | 30.25% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

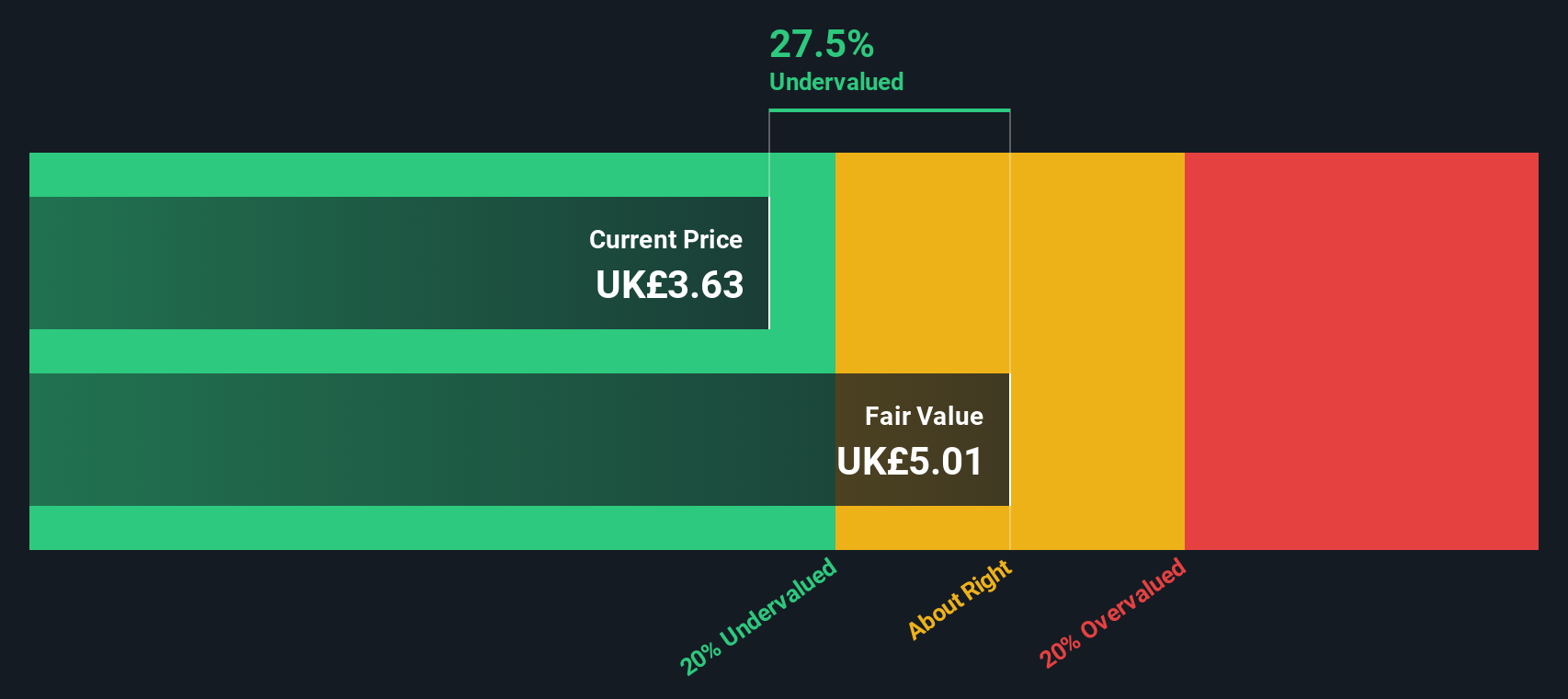

Hollywood Bowl Group (LSE:BOWL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Hollywood Bowl Group operates a chain of ten-pin bowling centers across the UK, focusing on providing family-friendly entertainment and leisure activities, with a market cap of approximately £0.63 billion.

Operations: The company generates revenue primarily from recreational activities, with a recent figure of £230.40 million. Its cost structure includes cost of goods sold and significant operating expenses, such as general and administrative costs. The gross profit margin has shown variability, most recently recorded at 63.15%.

PE: 15.6x

Hollywood Bowl Group, a smaller European stock, is catching attention for its potential value. Their earnings are projected to grow 11.45% annually. Despite relying solely on external borrowing, which poses higher risk, insider confidence is evident with Peter Boddy purchasing 100,000 shares for £320K in January 2025. The company initiated a share buyback program on February 18, allowing repurchase of up to 10% of its issued capital until March 2026.

Bytes Technology Group (LSE:BYIT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Bytes Technology Group is an IT solutions provider with a market cap of approximately £1.02 billion, focusing on delivering software, cloud services, and digital transformation solutions to various industries.

Operations: The company's revenue primarily comes from its IT solutions segment, with a gross profit margin reaching 74.86% by August 2024. Operating expenses have shown an upward trend, impacting net income margins which were at 25.47% for the same period.

PE: 22.9x

Bytes Technology Group, a European tech player, is attracting attention due to insider confidence shown through recent share purchases in early 2025. Despite relying entirely on external borrowing for funding, which carries inherent risks, the company's earnings are projected to grow at an annual rate of 7.62%. This growth potential coupled with insider activity suggests optimism about its future performance. As a small cap stock within Europe, Bytes presents an intriguing opportunity for those exploring underappreciated equities in the tech sector.

- Click here to discover the nuances of Bytes Technology Group with our detailed analytical valuation report.

Assess Bytes Technology Group's past performance with our detailed historical performance reports.

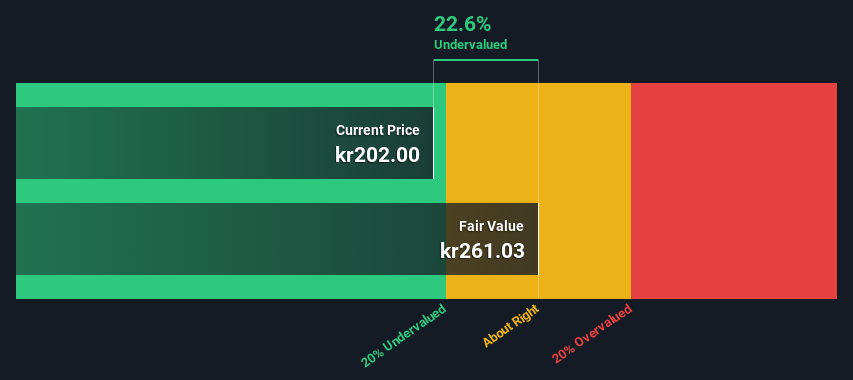

Sparebanken Sør (OB:SOR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Sparebanken Sør is a Norwegian financial institution offering a range of banking services, with operations in retail and corporate markets, and has a market capitalization of NOK 8.56 billion.

Operations: The primary revenue streams for the company are derived from the Retail Market (NOK 1.68 billion) and Corporate Market (NOK 1.32 billion). Operating expenses have shown an upward trend, reaching NOK 1.36 billion by the end of 2024. The net income margin has fluctuated over time, with a notable increase to approximately 20% by late 2024.

PE: 11.5x

Sparebanken Sør, a smaller player in the European financial sector, showcases potential for growth with earnings projected to rise by 34% annually. Despite relying on external borrowing for 53% of its liabilities, it maintains a low bad loan allowance at 32%. Recent financial results highlight an increase in net interest income to NOK 3.35 billion and net income to NOK 1.99 billion for 2024. Insider confidence is evident through recent share purchases, suggesting positive sentiment towards future prospects.

- Take a closer look at Sparebanken Sør's potential here in our valuation report.

Examine Sparebanken Sør's past performance report to understand how it has performed in the past.

Make It Happen

- Gain an insight into the universe of 64 Undervalued European Small Caps With Insider Buying by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hollywood Bowl Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:BOWL

Hollywood Bowl Group

Operates ten-pin bowling and mini-golf centers in the United Kingdom and internationally.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor