Advertisement

While small-cap stocks, such as Eckoh plc (LON:ECK) with its market cap of UK£95m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Companies operating in the IT industry, even ones that are profitable, are inclined towards being higher risk. Evaluating financial health as part of your investment thesis is crucial. Here are a few basic checks that are good enough to have a broad overview of the company’s financial strength. Though, this commentary is still very high-level, so I recommend you dig deeper yourself into ECK here.

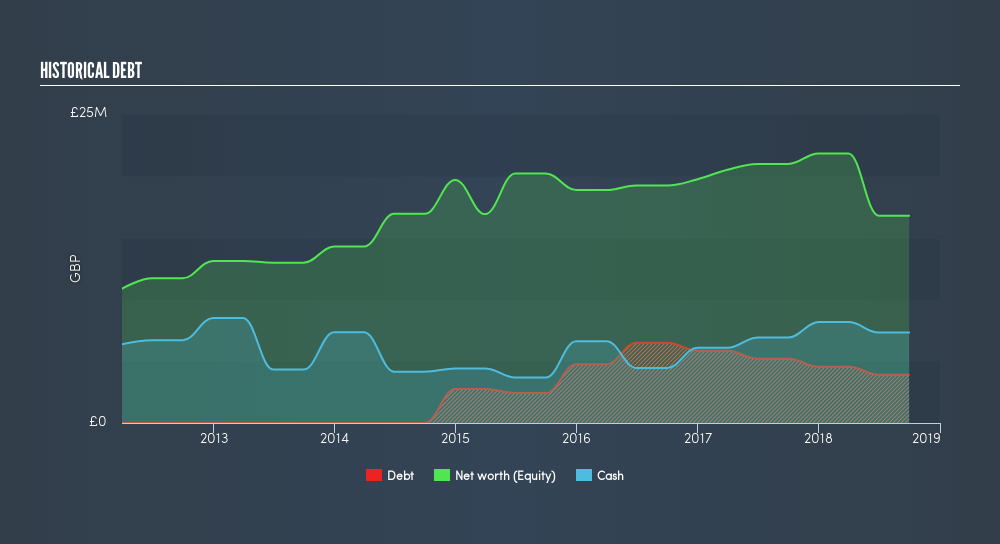

How does ECK’s operating cash flow stack up against its debt?

ECK's debt levels have fallen from UK£5.2m to UK£3.9m over the last 12 months , which includes long-term debt. With this debt repayment, the current cash and short-term investment levels stands at UK£7.3m for investing into the business. Moreover, ECK has produced cash from operations of UK£4.3m over the same time period, leading to an operating cash to total debt ratio of 110%, indicating that ECK’s operating cash is sufficient to cover its debt. This ratio can also be a sign of operational efficiency as an alternative to return on assets. In ECK’s case, it is able to generate 1.1x cash from its debt capital.

Can ECK pay its short-term liabilities?

With current liabilities at UK£18m, it appears that the company has been able to meet these obligations given the level of current assets of UK£22m, with a current ratio of 1.23x. For IT companies, this ratio is within a sensible range as there's enough of a cash buffer without holding too much capital in low return investments.

Does ECK face the risk of succumbing to its debt-load?

With debt at 23% of equity, ECK may be thought of as appropriately levered. This range is considered safe as ECK is not taking on too much debt obligation, which can be restrictive and risky for equity-holders. We can test if ECK’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings before interest and tax (EBIT) should cover net interest by at least three times. For ECK, the ratio of 32.42x suggests that interest is comfortably covered, which means that lenders may be less hesitant to lend out more funding as ECK’s high interest coverage is seen as responsible and safe practice.

Next Steps:

ECK’s debt level is appropriate for a company its size, and it is also able to generate sufficient cash flow coverage, meaning it has been able to put its debt in good use. Furthermore, the company exhibits an ability to meet its near term obligations should an adverse event occur. This is only a rough assessment of financial health, and I'm sure ECK has company-specific issues impacting its capital structure decisions. I recommend you continue to research Eckoh to get a more holistic view of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for ECK’s future growth? Take a look at our free research report of analyst consensus for ECK’s outlook.

- Valuation: What is ECK worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether ECK is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About AIM:ECK

Eckoh

Provides customer engagement data and payment security solutions in the United Kingdom, the United States, Canada, Ireland, and internationally.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor