Advertisement

While Inchcape plc (LON:INCH) might not be the most widely known stock at the moment, it led the LSE gainers with a relatively large price hike in the past couple of weeks. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, what if the stock is still a bargain? Today I will analyse the most recent data on Inchcape’s outlook and valuation to see if the opportunity still exists.

Our analysis indicates that INCH is potentially undervalued!

What's The Opportunity In Inchcape?

Inchcape appears to be overvalued by 27% at the moment, based on my discounted cash flow valuation. The stock is currently priced at UK£8.28 on the market compared to my intrinsic value of £6.49. This means that the opportunity to buy Inchcape at a good price has disappeared! If you like the stock, you may want to keep an eye out for a potential price decline in the future. Since Inchcape’s share price is quite volatile, this could mean it can sink lower (or rise even further) in the future, giving us another chance to invest. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

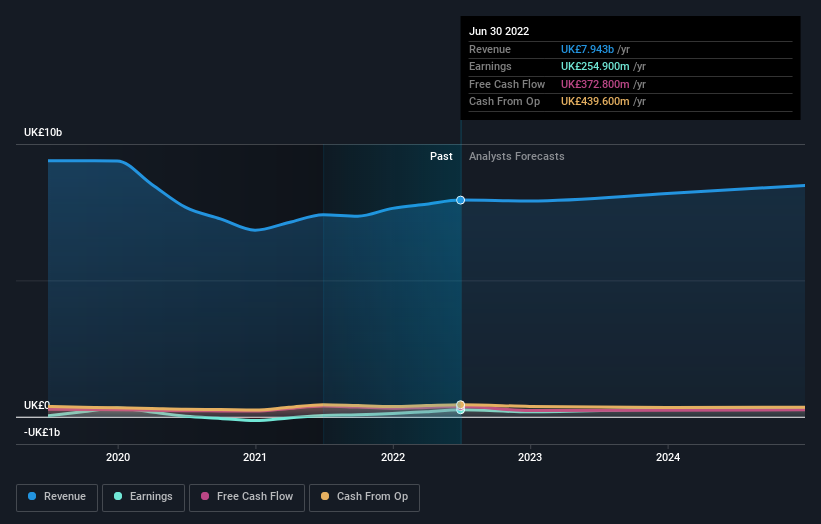

What kind of growth will Inchcape generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Though in the case of Inchcape, it is expected to deliver a relatively unexciting earnings growth of 8.6%, which doesn’t help build up its investment thesis. Growth doesn’t appear to be a main reason for a buy decision for the company, at least in the near term.

What This Means For You

Are you a shareholder? INCH’s future growth appears to have been factored into the current share price, with shares trading above its fair value. At this current price, shareholders may be asking a different question – should I sell? If you believe INCH should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on INCH for some time, now may not be the best time to enter into the stock. The price has surpassed its true value, which means there’s no upside from mispricing. However, the positive outlook means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

If you'd like to know more about Inchcape as a business, it's important to be aware of any risks it's facing. You'd be interested to know, that we found 3 warning signs for Inchcape and you'll want to know about these.

If you are no longer interested in Inchcape, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:INCH

Undervalued with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor