Advertisement

- United Kingdom

- /

- Office REITs

- /

- LSE:WKP

Time To Worry? Analysts Just Downgraded Their Workspace Group plc (LON:WKP) Outlook

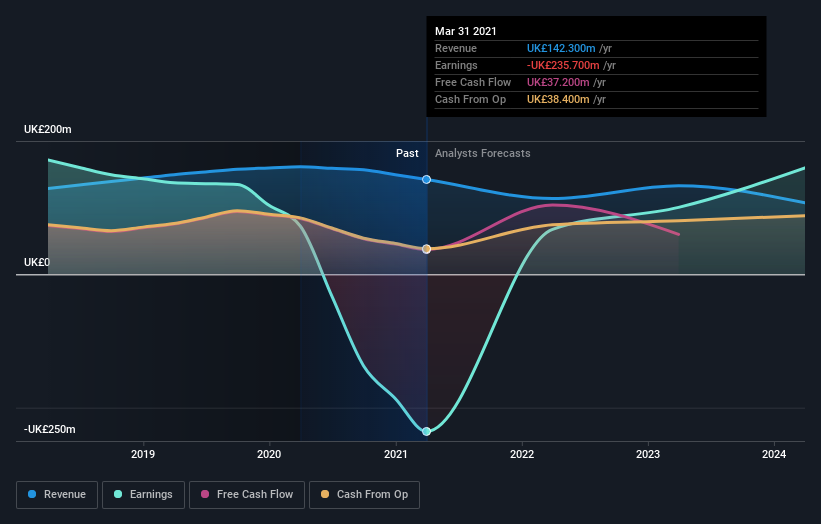

The analysts covering Workspace Group plc (LON:WKP) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue estimates were cut sharply as analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

Following the latest downgrade, the current consensus, from the four analysts covering Workspace Group, is for revenues of UK£114m in 2022, which would reflect a disturbing 20% reduction in Workspace Group's sales over the past 12 months. Before the latest update, the analysts were foreseeing UK£151m of revenue in 2022. The consensus view seems to have become more pessimistic on Workspace Group, noting the sizeable cut to revenue estimates in this update.

View our latest analysis for Workspace Group

The consensus price target rose 7.2% to UK£8.57, with the analysts clearly more optimistic about Workspace Group's prospects following this update. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Workspace Group at UK£10.25 per share, while the most bearish prices it at UK£6.70. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 20% by the end of 2022. This indicates a significant reduction from annual growth of 9.1% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.3% annually for the foreseeable future. It's pretty clear that Workspace Group's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They're also anticipating slower revenue growth than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Given the stark change in sentiment, we'd understand if investors became more cautious on Workspace Group after today.

Of course, there's always more to the story. At least one of Workspace Group's four analysts has provided estimates out to 2024, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade Workspace Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Workspace Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:WKP

Workspace Group

Workspace is London’s leading owner and operator of flexible workspace, currently managing 4.3 million sq.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.6% undervalued

MA

Community Contributor