Advertisement

Christopher Williams became the CEO of Wynnstay Properties Plc (LON:WSP) in 2006, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Wynnstay Properties.

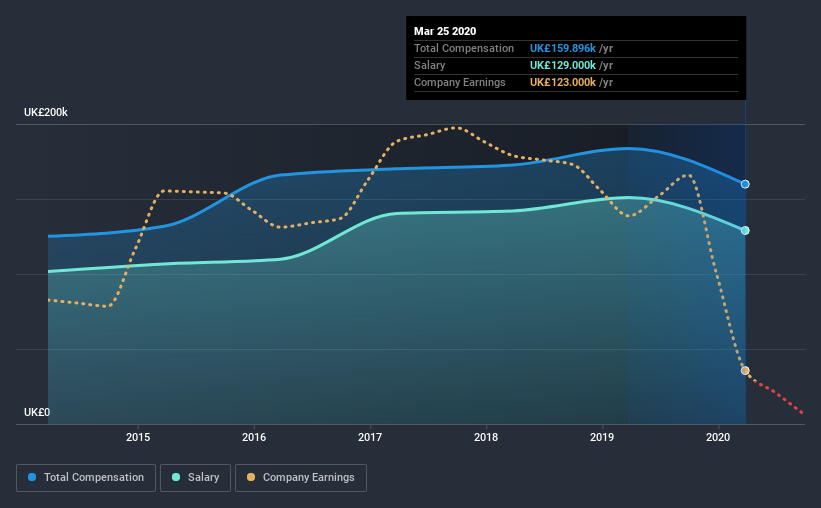

See our latest analysis for Wynnstay Properties

How Does Total Compensation For Christopher Williams Compare With Other Companies In The Industry?

At the time of writing, our data shows that Wynnstay Properties Plc has a market capitalization of UK£15m, and reported total annual CEO compensation of UK£160k for the year to March 2020. That's a notable decrease of 13% on last year. Notably, the salary which is UK£129.0k, represents most of the total compensation being paid.

On comparing similar-sized companies in the industry with market capitalizations below UK£145m, we found that the median total CEO compensation was UK£321k. This suggests that Christopher Williams is paid below the industry median. Furthermore, Christopher Williams directly owns UK£66k worth of shares in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£129k | UK£151k | 81% |

| Other | UK£31k | UK£33k | 19% |

| Total Compensation | UK£160k | UK£184k | 100% |

Speaking on an industry level, nearly 51% of total compensation represents salary, while the remainder of 49% is other remuneration. Wynnstay Properties is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Wynnstay Properties Plc's Growth

Wynnstay Properties Plc has reduced its earnings per share by 58% a year over the last three years. It saw its revenue drop 8.5% over the last year.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Wynnstay Properties Plc Been A Good Investment?

Wynnstay Properties Plc has not done too badly by shareholders, with a total return of 9.6%, over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

As we noted earlier, Wynnstay Properties pays its CEO lower than the norm for similar-sized companies belonging to the same industry. Over the last three years, shareholder returns have been unexciting, and EPS growth has fared even worse. So, although we can't say CEO compensation is very high, shareholders might want to see an improvement in overall performance before agreeing that Christopher deserves a bump.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 5 warning signs for Wynnstay Properties (of which 2 make us uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Wynnstay Properties or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wynnstay Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:WSP

Wynnstay Properties

Engages in the investment, development, and management of properties in the United Kingdom.

Average dividend payer with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative