Advertisement

- United Kingdom

- /

- Airlines

- /

- LSE:WIZZ

Discover August 2024's Top Undervalued Small Caps With Insider Buying In United Kingdom

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom market has recently been impacted by weak trade data from China, causing the FTSE 100 to close lower. Amid this broader market sentiment, identifying undervalued small-cap stocks with insider buying can present unique opportunities for investors looking to navigate these challenging conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 24.8x | 5.6x | 12.25% | ★★★★★☆ |

| Essentra | 849.8x | 1.6x | 47.16% | ★★★★★☆ |

| GB Group | NA | 3.1x | 32.30% | ★★★★★☆ |

| Norcros | 7.4x | 0.5x | 4.21% | ★★★★☆☆ |

| NWF Group | 9.1x | 0.1x | 32.45% | ★★★★☆☆ |

| Harworth Group | 14.0x | 7.4x | -516.90% | ★★★★☆☆ |

| CVS Group | 22.7x | 1.3x | 39.80% | ★★★★☆☆ |

| Watkin Jones | NA | 0.2x | 4.60% | ★★★★☆☆ |

| Foxtons Group | 26.8x | 1.3x | 46.87% | ★★★☆☆☆ |

| Franchise Brands | 116.8x | 2.9x | 48.85% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

Domino's Pizza Group (LSE:DOM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Domino's Pizza Group operates a network of franchise and corporate pizza stores, generating income from sales to franchisees, corporate stores, advertising and ecommerce, rental properties, and various fees; the company has a market cap of approximately £1.50 billion.

Operations: The company's revenue streams include sales to franchisees, corporate store income, national advertising and ecommerce income, rental income on leasehold and freehold property, and royalties and franchise fees. The gross profit margin has shown an upward trend from 36.25% in September 2013 to 47.48% in June 2024.

PE: 15.6x

Domino's Pizza Group, a small company in the UK, has shown insider confidence with share purchases from January to May 2024. Despite a drop in net income from £80.2 million to £42.3 million for H1 2024, earnings are forecasted to grow by 10.27% annually. The company repurchased 25.3 million shares worth £90.1 million and declared an interim dividend of 3.5p per share payable on September 27, 2024, indicating continued shareholder returns amidst strategic initiatives for growth in order count and sales

- Get an in-depth perspective on Domino's Pizza Group's performance by reading our valuation report here.

Evaluate Domino's Pizza Group's historical performance by accessing our past performance report.

Sirius Real Estate (LSE:SRE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Sirius Real Estate specializes in owning and operating business parks, industrial complexes, and office spaces across Germany and the UK, with a market cap of approximately €1.50 billion.

Operations: Sirius Real Estate generates revenue primarily from property investments, with a gross profit margin of 57.50% as of the latest reporting period. The company's cost structure includes significant operating expenses and non-operating expenses, impacting its net income margin which stands at 37.25%.

PE: 16.2x

Sirius Real Estate recently completed a £152.5 million follow-on equity offering, bolstering its acquisition strategy in Germany and the U.K. The company reported full-year earnings of €107.8 million, up from €79.6 million last year, showcasing solid growth. They declared a dividend increase for the six-month period ending March 2024 to €0.0305 per share, reflecting consistent performance improvements. Insider confidence is evident with significant insider buying activity throughout 2024, indicating strong belief in future prospects.

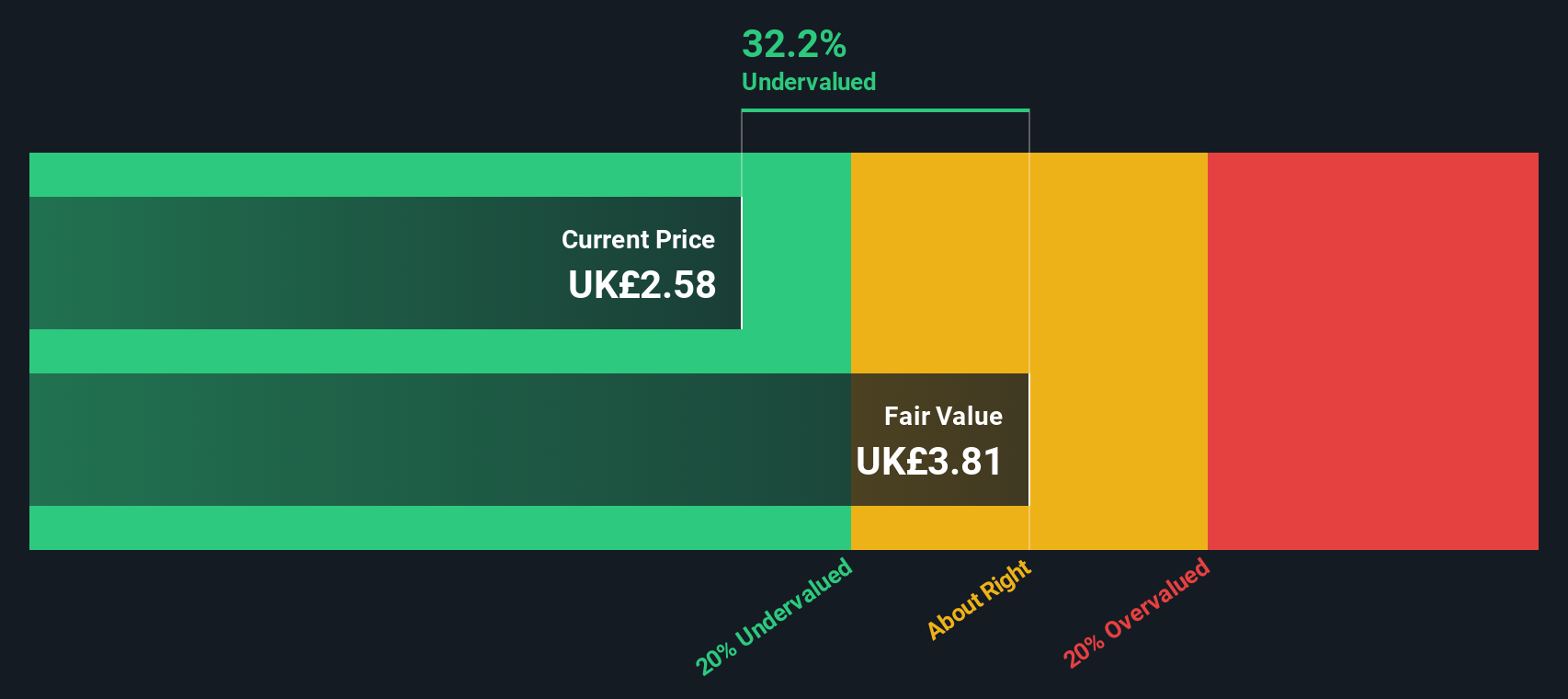

Wizz Air Holdings (LSE:WIZZ)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Wizz Air Holdings is a low-cost airline operating across Europe and parts of the Middle East with a market cap of approximately £2.82 billion.

Operations: Wizz Air Holdings generates revenue primarily from its route network, with the latest recorded revenue at €5095.8 million. The company has shown a notable gross profit margin trend, reaching 33.12% in March 2019 and standing at 22.49% by June 2024. Operating expenses include significant costs such as depreciation and amortization (€828.5 million) and sales & marketing (€117.3 million).

PE: 5.2x

Wizz Air Holdings, a notable player among smaller UK stocks, recently reported first-quarter revenue of €1.26 billion, up slightly from €1.24 billion a year ago, though net income dropped to €5.8 million from €62.8 million. The company's load factor for July 2024 was 93.8%, down from 94.9% the previous year, but it maintained stable annual figures with a load factor of 90%. Insider confidence is evident as executives purchased shares over the past six months, signaling potential growth ahead despite recent earnings volatility and leadership changes set for October 2024.

- Click to explore a detailed breakdown of our findings in Wizz Air Holdings' valuation report.

Assess Wizz Air Holdings' past performance with our detailed historical performance reports.

Next Steps

- Delve into our full catalog of 29 Undervalued UK Small Caps With Insider Buying here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wizz Air Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:WIZZ

Wizz Air Holdings

Engages in the provision of passenger air transportation services in Europe, Iceland, Liechtenstein, Norway, and Switzerland, the United Kingdom, and Other European countries.

Good value low.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor