Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that DeepVerge plc (LON:DVRG) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for DeepVerge

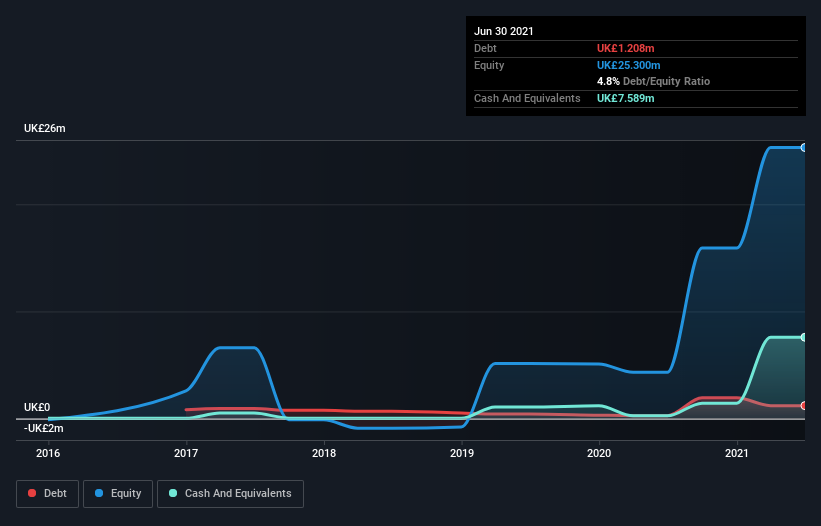

What Is DeepVerge's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of June 2021 DeepVerge had UK£1.21m of debt, an increase on UK£275.0k, over one year. However, its balance sheet shows it holds UK£7.59m in cash, so it actually has UK£6.38m net cash.

How Strong Is DeepVerge's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that DeepVerge had liabilities of UK£4.16m due within 12 months and liabilities of UK£4.31m due beyond that. Offsetting this, it had UK£7.59m in cash and UK£2.22m in receivables that were due within 12 months. So it actually has UK£1.34m more liquid assets than total liabilities.

This surplus suggests that DeepVerge has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that DeepVerge has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since DeepVerge will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year DeepVerge wasn't profitable at an EBIT level, but managed to grow its revenue by 359%, to UK£6.8m. When it comes to revenue growth, that's like nailing the game winning 3-pointer!

So How Risky Is DeepVerge?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months DeepVerge lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of UK£6.0m and booked a UK£4.2m accounting loss. Given it only has net cash of UK£6.38m, the company may need to raise more capital if it doesn't reach break-even soon. Importantly, DeepVerge's revenue growth is hot to trot. High growth pre-profit companies may well be risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for DeepVerge you should be aware of, and 3 of them can't be ignored.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:DVRG

DeepVerge

DeepVerge plc, an environmental and life science artificial intelligent company, develops and applies AI and IoT technology to analytical instruments for the analysis and identification of bacteria, virus, and toxins.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor