Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Avacta Group Plc (LON:AVCT) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Avacta Group

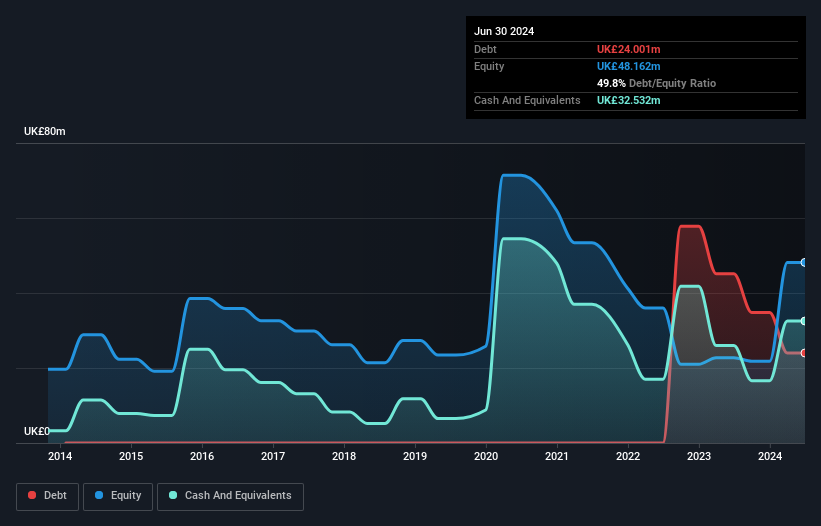

What Is Avacta Group's Debt?

You can click the graphic below for the historical numbers, but it shows that Avacta Group had UK£24.0m of debt in June 2024, down from UK£45.2m, one year before. But it also has UK£32.5m in cash to offset that, meaning it has UK£8.53m net cash.

How Healthy Is Avacta Group's Balance Sheet?

According to the last reported balance sheet, Avacta Group had liabilities of UK£35.3m due within 12 months, and liabilities of UK£5.87m due beyond 12 months. Offsetting these obligations, it had cash of UK£32.5m as well as receivables valued at UK£10.3m due within 12 months. So it can boast UK£1.71m more liquid assets than total liabilities.

Having regard to Avacta Group's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the UK£203.1m company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Avacta Group boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Avacta Group can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Avacta Group wasn't profitable at an EBIT level, but managed to grow its revenue by 41%, to UK£23m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Avacta Group?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Avacta Group had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through UK£21m of cash and made a loss of UK£26m. But at least it has UK£8.53m on the balance sheet to spend on growth, near-term. With very solid revenue growth in the last year, Avacta Group may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 5 warning signs for Avacta Group you should be aware of, and 3 of them are potentially serious.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:AVCT

Avacta Group

Engages in the development of cancer therapies in the United Kingdom, South Korea, and internationally.

Moderate with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor